Current enforcement practice does not consider how mergers alter the

merging parties’ incentives to petition for trade protection. I document

mergers between domestic producers across jurisdictions that are

followed by tariff petitions. I develop a model to characterize the

trade-policy channel of mergers. Theoretically, a domestic merger raises

the profitability of tariffs when offshoring is unavailable; once

offshoring is possible, the effect becomes ambiguous. I apply this

framework to a merger between domestic producers in the U.S. appliance

industry. Empirically, I find that when import competition is weak, the

merging parties prefer to lower their own costs through offshoring; when

import competition is strong, the merger makes it more profitable for

them to raise their foreign rivals’ costs through tariffs. The resulting

consumer harm is comparable in magnitude to the direct market-power

effect. A hypothetical cross-border merger reduces the profitability of

tariffs in this market.

Mergers and the Demand for Protectionism

Felix Montag

NYU Stern,

CEPREmail:

felix.montag@nyu.edu. I thank Jonathan Elliott, Karam Kang, and Ali

Yurukoglu, as well as seminar participants at NYU, the Stigler Center,

the ITAM/UT Austin IO Conference, Georgetown University and the Yale

Trade Day for helpful comments and suggestions. This work was supported

in part through the NYU IT High Performance Computing resources,

services, and staff expertise.

This version: 2026-06-10

Introduction

Antitrust enforcement in most jurisdictions, including the European

Union and the United States, applies a consumer-welfare standard. This

standard is administered separately from trade policy, keeping antitrust

focused on consumer welfare and insulated from trade-policy

considerations (Bradford and Chilton 2021). As trade

costs fall, lowering costs through offshoring becomes more profitable

for domestic incumbents and increases their support for free trade. At

the same time, if domestic producers are subject to intense import

competition, domestic consolidation may raise their demand for

protectionism.

Antidumping (AD) and countervailing duty (CVD) petitions are the most

common ways domestic producers seek trade protection. The investigating

authority subjects imports to tariffs if it determines that they are

sold at less than fair value or subsidized by a foreign government, and

that the domestic industry is materially injured by those imports. The

mandate of the investigating authority can conflict with the competition

authority’s consumer-welfare

standard.Recognizing

this tension, in 2022 the U.S. Senate Subcommittee on Competition

Policy, Antitrust, and Consumer Rights asked the U.S. Government

Accountability Office to review AD/CVD processes and domestic market

competition considerations, particularly focusing on “how aspects of

market competition factor into the AD/CVD process” (U.S. Government Accountability

Office 2022). Despite this potential conflict, the

trade-policy implications of mergers remain unexamined in clearance

decisions. Across multiple jurisdictions, I identify high-profile

horizontal mergers between domestic producers followed by tariff

petitions. In many of the corresponding merger clearance decisions,

imports are mentioned as a competitive constraint on the merging

parties.

In this paper, I study how merger control affects domestic

incumbents’ incentives to petition for tariffs. I develop a framework to

estimate whether a proposed merger lowers or raises the profitability of

tariffs to the merging parties, and hence their propensity to file. I

apply this framework to the Whirlpool–Maytag merger in the U.S.

appliance industry, specifying and estimating a structural model of

demand and supply following Montag (2026), with which I quantify the

effect of the domestic merger across counterfactual production-location

scenarios. To examine the effect of cross-border mergers, I also

quantify how a hypothetical merger between Whirlpool and LG changes the

profitability of tariff petitions.

The paper’s central contribution is to identify and quantify a

trade-policy channel through which mergers between domestic producers

can harm consumers beyond direct market-power effects. Theoretically,

when offshoring is unavailable, a domestic merger strictly raises the

profitability of tariffs to the merging parties; when offshoring is

available, the sign becomes ambiguous. Empirically, I find that for the

Whirlpool–Maytag merger, offshoring is more profitable than petitioning

for tariffs in years when import competition is weak, while petitioning

becomes more profitable than offshoring in years when import competition

is strong. Even holding the likelihood of tariffs fixed, the merger

raises tariff-induced consumer harm by more than 10 percent; in total,

the consumer harm through the trade-policy channel is of the same order

of magnitude as the harm from unilateral market power. A hypothetical

cross-border merger reduces the profitability of tariffs in the same

market.

I specify a three-stage model to analyze the effect of mergers on the

incentives to petition for tariffs. In Stage 1, the competition

authority adjudicates a horizontal merger involving a domestic incumbent

that faces import competition. In Stage 2, given the competition

authority’s decision, the incumbent chooses among offshoring production

to lower marginal costs, petitioning for tariffs to raise foreign

rivals’ costs, or maintaining the status

quo.Igami (2018) studies the

relationship between import competition and offshoring in the Hard Disk

Drive Industry, showing that offshoring is pro-competitive and benefits

consumers. Stage 3 embeds a differentiated-demand,

oligopolistic-supply model in which firms set prices and consumers

choose products.

Most directly, the paper relates to a literature concerned with the

stringency of merger control. Nocke and Whinston (2022) show that

current concentration thresholds are too lax in the absence of large

efficiency gains. Retrospective analyses of consummated mergers found

mixed results (Ashenfelter et

al. 2013; Kwoka 2015; Bhattacharya et al. forthcoming). Asker and Nocke (2021)

and Shapiro and

Yurukoglu (2026) review this literature and conclude that the

estimated price effects vary widely and that the evidence is mixed.

Breinlich et al.

(2018) study optimal merger policy for international mergers in

settings where multiple national agencies can block a transaction across

jurisdictions.Horn and Levinsohn (2001)

and De Stefano and

Rysman (2010) develop models in which a country chooses the level

of domestic concentration through merger policy and show that when firms

are exporters, national authorities may prefer a level of concentration

that is excessive from a global perspective.Montag (2026) extends

the scope of merger analysis by studying how the Whirlpool–Maytag merger

affects total domestic welfare (consumers and workers) when potential

acquirers for Maytag differ in their offshoring plans.

I extend this literature by identifying a channel through which

mergers affect consumers via trade policy: by changing the merging

parties’ incentives to raise rivals’ costs through tariff

petitions.Salop et al. (1984)

discuss how tariffs can be used to raise the cost of rivals.

Furthermore, I provide a quantitative framework that allows competition

authorities to assess how a merger changes the profitability of tariffs

for the merging parties and the resulting consumer harm. I show that

imports impose weaker competitive discipline on a merged domestic

incumbent than equivalent domestic rivals would: because imports can be

restricted through trade remedies but domestic rivals cannot, the

discipline-from-imports defense for merger clearance can be weaker than

it

appears.This

limits the widely held presumption, formally examined by Neven and Seabright

(1997), that trade liberalization can substitute for domestic

competition policy. The stronger the competitive constraint from

imports, the stronger the incentive to petition for trade remedies.

Merger control should therefore discount the competitive constraint from

imports when this can be restricted post-merger.

The paper also contributes to a literature on market structure and

lobbying. Classic political-economy models predict that organized

sectors obtain protection (Grossman and Helpman 1994;

Goldberg and Maggi 1999), and firm size predicts participation

and intensity (Bombardini 2008). Kang (2016) finds that

while lobbying has a small effect on policy enactment, the returns to

lobbying are high. Recent evidence indicates that consolidation raises

lobbying across (Cowgill

et al. 2024) and within industries (Moshary and Slattery 2024).

I contribute to this literature in two ways. First, I extend it

beyond traditional political lobbying. AD/CVD petitions are a

quasi-judicial channel, relatively insulated from direct political

bargaining, that present incumbents with a distinct choice set

(petition, offshore, or maintain the status quo). I show that mergers

between domestic producers raise the profitability of tariffs for the

merging parties. Second, I decompose the merger effect into two

channels: the appropriation effect (the acquirer internalizes

the benefits of tariffs to the target) and the strategic effect

(the tariff raises the profit of the merged firm by more than the sum of

standalone

profits).While

domestic producers could overcome the collective-action problem by

petitioning together, in practice, they often do not. Bombardini and Trebbi

(2012) find that firms in more concentrated industries are more

likely to lobby on trade issues individually rather than through a trade

association. Distinguishing them matters because the two channels

respond differently to the merger structure.

A related literature studies how AD/CVD cases can raise market power

(Nieberding

1999; Konings and Vandenbussche 2005; Pierce 2011; Rovegno 2013)

and facilitate collusion (Staiger and Wolak 1989). Because

dumping margins depend on foreign pricing, the option value of a

petition can induce higher foreign prices even before a case is filed.

Blonigen et al.

(2013) find that binding quotas increased market power in the

U.S. steel industry, whereas tariffs did not, which is consistent with

strong domestic competition from minimill producers disciplining

outcomes. Flaaen et al.

(2020) show that the initial AD/CVD actions on large residential

washers primarily induced tariff jumping, whereas the 2018 global

safeguards raised U.S. washer prices.

I extend this literature to show that when there are few domestic

competitors, tariffs can generate substantial consumer harm. Whereas the

literature focuses on how protection changes competition, I focus on how

mergers alter the likelihood and harm from tariffs.

The Draghi

(2024) report argues that European economic growth requires scale

economies, prompting calls to relax EU merger

control.Even

earlier, France and Germany urged approval of the Siemens/Alstom merger

to create a “European champion” in rail equipment; the European

Commission nonetheless blocked the transaction in 2019. The

European Commission’s April 2026 Draft Merger Guidelines also emphasize

the enablement of scale economies. My results do not imply that merger

control should be tightened across the board. Instead, mergers between

domestic firms facing strong import competition should be scrutinized

more closely; cross-border consolidation, by contrast, can deliver scale

economies without raising incumbents’ returns to tariff petitions.

The remainder is structured as follows: Section 2 reviews measures to protect against

import competition and their relation to merger control, Section 3 specifies the model, Section 4 describes the appliance industry,

Section 5 details the empirical model and

estimation, Section 6 presents the parameter estimates,

Section 7 simulates counterfactuals, and

Section 8 concludes.

Trade Protection and Merger Control

AD and CVD measures are the most commonly used trade-defense

instruments worldwide. Since these are grounded in World Trade

Organization (WTO) rules, the criteria and procedures for AD/CVD are

codified in WTO agreements and apply across WTO members. Global

safeguards (GS) are also WTO-authorized but used much less frequently.

While the following discussion focuses on the institutional

implementation in the United States, it should be understood as applying

to other jurisdictions as well.

In the United States, the most commonly used alternative

trade-defense tools are Section 232 actions (national security-based

trade measures) and Section 301 actions (retaliatory trade measures). In

the U.S., AD/CVD measures accounted for 97 percent of all trade actions

initiated between 2002 and 2024 and in 2022 resulted in tariffs covering

$37.4 billion of imports (Liu 2026). AD/CVD almost always originate

from a petition filed by a domestic stakeholder. In contrast,

Section 232 and Section 301 actions are initiated by the government and

are not grounded in WTO authorized procedures. Based on interviews with

practitioners, Liu

(2026) reports that AD/CVD petitions remain the first tool of

choice for domestic producers seeking protection from import

competition.

AD duties are imposed on imports that are determined to be sold at

less than fair value and that materially injure a domestic industry.

Selling at less than fair value typically refers to a situation in which

a firm sells a product at a lower price in the importing country than in

its home market (Blonigen and Prusa 2016). If the

exporter’s home market is deemed unsuitable for comparison, its sales

price in a third country may be used instead. Since products destined

for home and export markets often differ, defining the foreign-like

product affords the Department of Commerce considerable leeway in AD

cases. An alternative standard used in many AD cases is sales below

cost. Although allocating fixed costs to products is notoriously

difficult and standard economic theory shows that firms may rationally

sell below average total cost (but above average variable cost), a price

below average total cost is considered

dumping.Blonigen and Prusa

(2016) explain that although the U.S. Antidumping Act of 1916 was

originally designed to protect domestic producers from predatory

pricing, the required predatory intent was soon dropped from the law,

and it has since become an ordinary protection tool.

While the U.S. International Trade Commission (USITC) may solicit

downstream purchaser information during its investigations, AD/CVD laws

do not allow the USITC to consider the economic effects of exporters’

behavior on downstream purchasers or on the national interest (U.S. Government Accountability

Office 2022). In practice, the Department of Commerce determines

whether the product is sold at less than fair value, and the USITC

determines whether a domestic industry is materially injured by reason

of the imports. In making the injury determination, the USITC cannot

take into account any potential harm that AD/CVD duties may impose on

downstream industries or consumers. This constraint lies at the core of

the tension between trade law and competition law. While federal

agencies, including the Department of Justice (DOJ) and the Federal

Trade Commission (FTC), can submit statements of interest in AD/CVD

cases, the DOJ has done so only once and promptly withdrew its

statement. No other federal agency has submitted a statement in recent

decades (U.S. Government

Accountability Office 2022). WTO rules do not impose this

constraint. Australia, Brazil, Canada, and the European Union all have

some form of public-interest provisions that can lower or eliminate

duties if doing so benefits downstream users.

AD is popular among domestic petitioners for several reasons. First,

AD is a particularly effective instrument against import competition

because it discourages exporters from competing aggressively: the lower

the exporter’s price, the more likely a domestic rival can establish

that the product is sold at less than fair value. Since the tariff rate

increases with the exporter’s productivity, Ruhl (2014) shows that AD is particularly

distortionary. Second, investigations last at most 18 months and the

clear criteria and quasi-judicial framework make them predictable and

more insulated from political interference (Blonigen and Prusa 2016). Third, while

AD duties require periodic review, many remain in effect for

decades.

CVD measures address cases in which imports are found to benefit from

foreign subsidies. As with AD, the imports must materially injure, or

threaten to materially injure, a domestic industry. Although the trade

practices targeted by AD and CVD differ, the procedures and underlying

concerns are often similar, and petitioners frequently seek protection

under both measures simultaneously (Liu 2026).

Unlike AD/CVD, global safeguards can be imposed on fairly traded

imports from all countries if a domestic industry is found to be

seriously injured by a surge in imports; they do not require evidence of

dumping or foreign subsidization. In the U.S., they are imposed at the

discretion of the President for an initial duration of up to four years.

They are therefore also more subject to the political process.

AD/CVD petitions occur frequently. According to data compiled by

Bown et al. (2025),

between 1980 and 2024 the EU initiated 440 AD, 77 CVD, and 7 GS

investigations, while India initiated 517, 24, and 48, respectively.

U.S. authorities initiated 747 AD, 453 CVD, and 15 GS investigations

during the same time period. Between 2011 and 2021, 74 percent of AD/CVD

petitions in the U.S. resulted in orders (U.S. Government Accountability Office

2022). At the same time, preparing a petition is costly,

requiring legal counsel, expert economic analysis, participation in

administrative hearings, as well as periodic sunset reviews.

Practitioners interviewed by Liu (2026) estimate that the cost of a

simple AD/CVD petition ranges between $1 million and $3 million, and can

be substantially higher for complex cases involving multiple products or

origin countries.

Petitions for trade remedies are typically initiated by domestic

firms or industry associations that claim injury from foreign

competition. Liu

(2026) reports 789 petitioner appearances in AD/CVD cases between

2002 and 2024, representing 528 unique entities. Of these, 14 were labor

unions, 217 were trade associations or coalitions, and the remaining 297

(56%) were individual domestic producers. In many cases, only a subset

of domestic producers participate in a petition. Although 55 percent of

petitioners are connected to the steel or chemicals industries,

petitions arise in many tradable-goods sectors.

While any domestic producer may petition for trade remedies, smaller

producers often cannot meet the statutory industry-support thresholds

required for filing and therefore cannot petition alone. According to

the WTO Antidumping Agreement’s industry-support thresholds, a petition

is deemed “on behalf of the industry” if its supporters account for at

least 25 percent of total domestic production of the domestic like

product and more than 50 percent of the production of those expressing a

view. When these thresholds are met, Commerce may initiate without

polling producers, thereby reducing procedural frictions and the risk of

standing challenges (United States

Code 2025b, 2025a; Code of Federal Regulations 2025; U.S. International

Trade Commission 2015).

To understand whether mergers are associated with trade-remedy

petitions, I assemble a non-representative sample of nine horizontal

mergers affecting 16 antitrust markets, where the merging parties have

domestic production capacity in the relevant antitrust markets and where

AD/CVD petitions were filed in at least one antitrust market within five

years

post-merger.The

mergers span aluminium extrusions in Australia; thermoplastic resins in

Brazil; oil country tubular goods in Canada and the United States;

continuous filament glass fibre, stainless steel, and graphic paper in

the European Union; flat-rolled carbon steel in India; and appliances in

the United States.

A more systematic descriptive analysis is constrained by data

availability. While data on AD/CVD petitions is publicly available and

aggregated by Bown et al.

(2025), information about market shares and the number of

domestic producers at the antitrust-market level is generally not

disclosed. For mergers that competition authorities scrutinize more

heavily, redacted versions of this information sometimes appear in the

published

decisions.This

is especially true for the European Commission, which publishes detailed

merger decisions that include lengthy discussions of market definition

for Phase II merger investigations. Crucially, the same

producer-share information is not available for the “control markets”

needed to construct a comparison

group.Section 4.3 takes an alternative approach,

exploiting variation across U.S. appliance markets where some experience

a fall in the number of domestic producers and others do not.

In many of these cases, the clearance decision explicitly cites

import competition as a competitive constraint on the merging parties.

Two of the sample cases illustrate the pattern. In its Owens Corning

/ Saint Gobain Vetrotex conditional approval, the European

Commission cites customer reports claiming that imports are a viable

alternative to domestic producers for certain types of rovings (European

Commission 2007). Two years after the merger, a group of domestic

producers, including Owens Corning, filed an AD petition on continuous

glass fibre from China, which includes rovings. In the United States,

the DOJ cleared the Whirlpool–Maytag merger on the grounds that foreign

manufacturers posed a sufficiently large competitive constraint to

prevent post-merger price increases (Department of Justice 2006). Once these

foreign manufacturers gained significant market shares, Whirlpool filed

for AD and CVD on large residential washers from Korea and Mexico.

While AD/CVD are sometimes discussed in merger cases, this is usually

in the context of how they shape the competitive environment. For

example, in its ArcelorMittal / Ilva decision, the European

Commission writes “As the trade defence measures on certain [...]

products cover some of the major steel producing and steel exporting

countries, any assessment of the extent to which imports of HR, CR and

HDG products may exert competitive pressure on EEA-based flat carbon

steel producers and, in particular the merged entity post-Transaction,

must be made in light of the situation as restored by anti-dumping

duties” (European Commission 2018,

56). The Commission thus treats the trade-defense environment as

an exogenous input to merger analysis, rather than considering how the

merger itself may alter the incentives to petition for new measures.

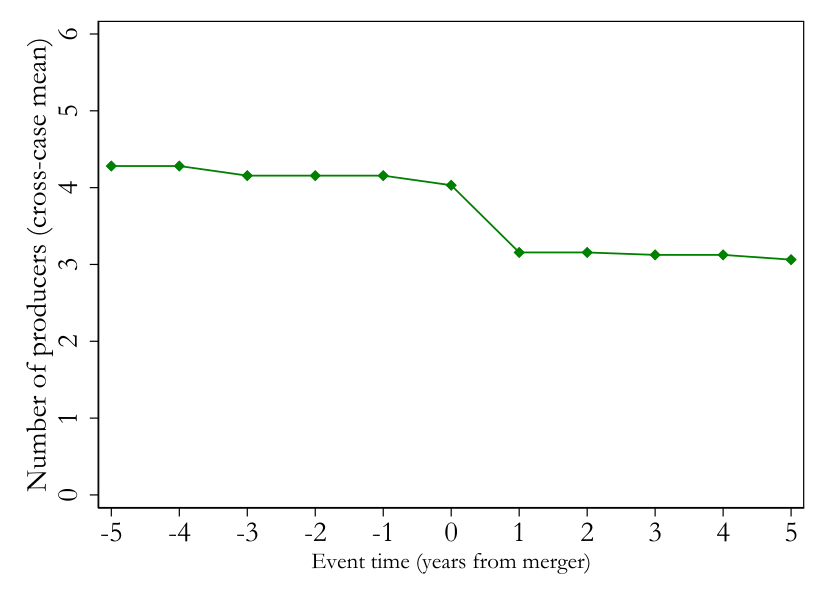

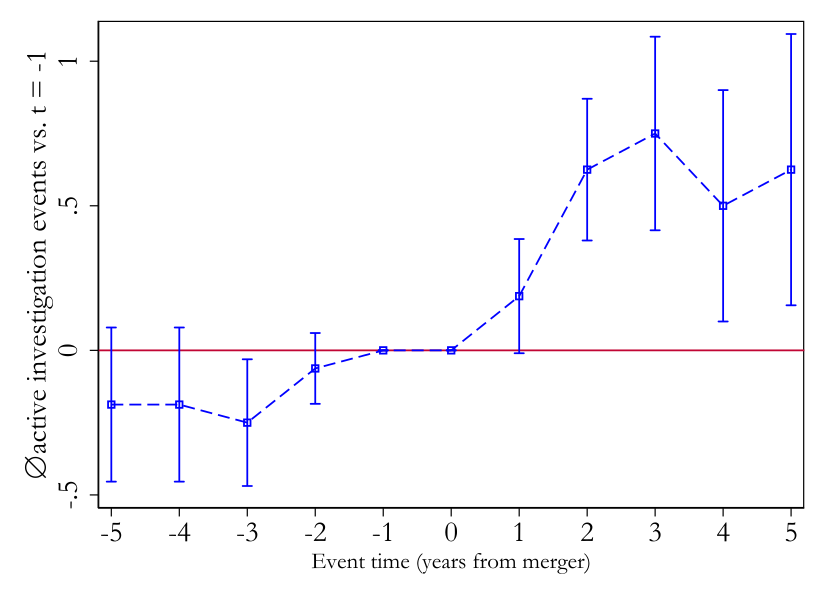

Figure 1 plots the number of

domestic producers that together account for at least \(80\%\) of domestic production (\(n^{80}_{jt}\)), as well as the average

within-market deviation of the number of active AD/CVD cases from its

pre-merger (\(t=-1\)) baseline, for the

nine horizontal mergers across 16

markets.Appendix 9 reports the per-case

concentration changes, restriction counts, and source

documentation. It shows that while the cross-case mean number of

major domestic producers decreases post-merger, the count of active

AD/CVD investigations increases.

A. Domestic concentration (\(n^{80}\))

B. AD/CVD restrictions

Notes: Panel A. Cross-case-product mean of \(n^{80}_{jt}\), the number of domestic

producers accounting for at least 80% of domestic production in the

affected product market in a particular year. Panel B.

Cross-case-product mean of the within-market deviation of the

active-restriction count in a particular year from its \(t = -1\) baseline. Whiskers show 95% CIs.

Mergers occur at \(t=0\).

Figure 1: Concentration and AD/CVD

restrictions around domestic mergers

Although this relationship is purely descriptive and could be caused

by other market trends affecting concentration and AD/CVD petitions, it

shows that in some mergers that are heavily scrutinized by antitrust

authorities, increases in domestic production concentration are followed

by increases in trade-remedy petitions.

In summary, AD/CVD cases are pervasive across the economy. The

administrative structure of the process makes petition outcomes

predictable, and success rates are higher when the foreign competitor

prices aggressively. Petitions are costly and are often filed by a

single domestic firm. Filing a petition therefore requires the

petitioner to expect sufficiently large increases in profits to offset

the cost of petitioning. Finally, mergers between domestic producers are

sometimes followed by trade-remedy petitions. The remainder of the paper

develops a model of merger-induced petitioning informed by these facts,

estimates it on the Whirlpool–Maytag case, and quantifies the resulting

consumer-welfare consequences.

Stylized Model

I specify a stylized model illustrating the link between mergers and

the demand for protectionism.

Setup

Consider a market with three firms. Firm 1 is a domestically

producing incumbent, firm 2 is a domestic acquisition target, and firm 3

is a foreign rival. Each firm produces a single, horizontally

differentiated product and sells exclusively in the domestic market.

Demand is generated by a unit mass of consumers with heterogeneous

preferences following a standard logit specification.

Each consumer derives utility from purchasing a single product or an

outside good. Products differ in product-specific deterministic utility

\(\delta_j\). The utility that a

consumer obtains from product \(j \in

\{1,2,3\}\) and from the outside option is \[\begin{equation}

\tag{1}

U_j = \delta_j - \alpha p_j + \varepsilon_j,

\qquad

U_0 = \varepsilon_0,

\label{eq:sty_utility}

\end{equation}\] where \(p_j\)

denotes the price of product \(j\),

\(\alpha > 0\) governs price

sensitivity, and \(\varepsilon_j,\varepsilon_0\) are

i.i.d. Type I extreme value.

Marginal cost depends on the location of production. Marginal cost is

\(c_D\) for domestic production and

\(c_F\) for foreign production, with

\(c_D>c_F\). Initially, firms 1 and

2 produce domestically at \(c_D\), and

firm 3 produces abroad at \(c_F\).

Relocation is a firm-level decision: firm \(f\) can relocate all of its production at a

fixed cost \(R_f>0\), paid once

regardless of the number of products it relocates. \(R_2\) is assumed to be high enough such

that firm 2 never relocates; \(R_1\) is

finite. If firm 1 acquires firm 2, it controls both products and, paying

\(R_1\) once, may relocate any

subset.

Firm 1 may petition for tariffs on all imports at petitioning cost

\(L>0\). If filed, the tariff is

imposed with certainty. The level of the ad valorem tariff \(\kappa>0\) is exogenously determined by

the trade commission and scales foreign marginal costs to \((1+\kappa)c_F\).

Stage 1: merger control

The domestic incumbent (firm 1) proposes a horizontal merger; let

\(\mathcal{M}\) denote the proposed

configuration. The competition authority (CA) applies a policy rule to

decide whether to clear or challenge. The CA’s baseline rule clears the

merger whenever the predicted change in consumer surplus from unilateral

market-power effects, \(\Delta^{MP}

CS(\mathcal{M})\), exceeds a policy threshold \(\bar{\Delta}\le 0\), the largest tolerated

reduction in consumer surplus: \[\begin{equation}

\tag{2}

\Delta^{MP} CS(\mathcal{M}) \;\ge\; \bar{\Delta}.

\label{eq:ca_rule}

\end{equation}\] In settings where horizontal mergers can alter

firms’ demand for trade protection, which translates into consumer

surplus through tariffs and prices, there is an additional trade-policy

channel of consumer surplus change, \(\Delta^{TP} CS(\mathcal{M})\), computed

from the equilibrium petitioning, offshoring, and pricing decisions

specified in Stages 2 and 3 below. If the CA evaluates mergers on

consumer welfare regardless of channel, it should apply the threshold to

the total effect, \(\Delta^{MP}

CS(\mathcal{M}) + \Delta^{TP} CS(\mathcal{M})\).

Stage 2: petitioning and

offshoring

Following the merger control decision, firm 1 decides whether to

offshore production, petition for tariffs, or maintain its current

production structure without petitioning. It chooses the option that

maximizes static profits net of fixed costs. Firm 1 never optimally

chooses to petition and offshore, because petitioning while offshoring

would raise firm 1’s own costs through the tariff.

If the merger is cleared, firm 1 prices products 1 and 2 jointly and

internalizes relocation and tariff effects across both products. If the

merger is blocked, firm 2 remains a separate domestic single-product

firm with cost \(c_D\) and never

relocates (since \(R_2\) is

sufficiently high).

Stage 3: pricing and demand

In the third stage, firms simultaneously choose prices in a

Bertrand-Nash equilibrium and consumers make discrete purchase

decisions.

Let \(s_j(\mathbf{p})\) denote the

logit market share of product \(j\)

implied by the utility specification above; \(s_0(\mathbf{p})\) is the outside share.

Given realized marginal costs \(c_j \in

\{c_D,c_F,(1+\kappa)c_F\}\) from Stage 2, each firm \(f\) chooses prices to maximize \(\sum_{j\in

\mathcal{J}_f}(p_j-c_j)s_j(\mathbf{p})\), where \(\mathcal{J}_f\) is the firm’s product set.

For a single-product firm \(j\), the

standard logit FOC gives \[\begin{equation}

\tag{3}

p_j=c_j+\frac{1}{\alpha(1-s_j)}.

\label{eq:sty_foc}

\end{equation}\] If firm 1 is multiproduct post-merger, prices

solve the following system of first-order conditions \[\begin{equation}

\tag{4}

\mathbf{p}=\mathbf{c}-\left(\frac{\partial \mathbf{s}}{\partial

\mathbf{p}}\circ\Omega\right)^{-1}\mathbf{s}(\mathbf{p}),\qquad

\frac{\partial s_j}{\partial p_k}=\begin{cases}

-\alpha s_j (1-s_j),& j=k,\\

\alpha s_j s_k,& j\neq k,

\end{cases}

\label{eq:sty_pricing}

\end{equation}\] where \(\mathbf{p}\), \(\mathbf{c}\), and \(\mathbf{s}(\mathbf{p})\) are the stacked

vectors of prices, costs, and shares, \(\partial \mathbf{s}/\partial \mathbf{p}\)

is the matrix of own- and cross-price share derivatives, \(\Omega\) is the ownership matrix with \(\Omega_{jk}=1\) if the same firm owns

products \(j\) and \(k\), and \(\circ\) denotes the Hadamard (element-wise)

product.

The consumer surplus change between two equilibria is the

compensating variation (Small and Rosen 1981): \[\begin{equation}

\tag{5}

\Delta

CS=\frac{1}{\alpha}\Big[\log\big(1+\textstyle\sum_{j}\exp(\delta_j-\alpha

p_j^{\text{after}})\big)-\log\big(1+\textstyle\sum_{j}\exp(\delta_j-\alpha

p_j^{\text{before}})\big)\Big].

\label{eq:sty_cs}

\end{equation}\]

Mergers, offshoring,

and trade protection

I now analyze the firms’ strategic choices in light of the merger

decision and the availability of trade-policy instruments. I focus on

how a merger between firms 1 and 2 affects firm 1’s incentive to

offshore production versus petition for trade protection, and how these

choices interact with market structure and consumer welfare. Proofs can

be found in Appendix 10.

Let \(\pi^{r}_{f,\mathcal{C}}\)

denote firm \(f\)’s variable profit in

regime \(r \in

\{\text{off},\text{pet},\text{sq}\}\) chosen by firm 1, under

merger configuration \(\mathcal{C} \in

\{\mathcal{S},\mathcal{M}\}\). \(\Pi^{r}_{f,\mathcal{C}}\) denotes total

profit, net of the relevant fixed cost. When the merger is cleared, firm

1 owns products 1 and 2; when blocked, it owns only product 1. For the

merged entity I drop the firm subscript and write \(\pi^{r}_{\mathcal{M}}\) and \(\Pi^{r}_{\mathcal{M}}\).

Proposition 1. Assume offshoring is more

profitable than petitioning at \(\kappa=0\), and petitioning is more

profitable than offshoring at some \(\hat{\kappa}>0\). Then there exists a

unique cutoff \(\kappa^* \in

(0,\hat{\kappa})\) such that firm 1 prefers petitioning over

offshoring iff \(\kappa>\kappa^*\).

A higher tariff raises foreign costs only, shifts shares toward firm

1, and increases its markups; offshoring leaves foreign costs unchanged

and lowers firm 1’s own costs. There is a unique \(\kappa^*\) at which firm 1 is indifferent,

above which it petitions and below which it offshores. The petitioning

payoff is monotonically increasing in \(\kappa\) while the offshoring payoff is

independent of \(\kappa\), giving a

unique crossing \(\kappa^*\).

To see how this threshold \(\kappa^*\) evolves with the competitiveness

of the foreign rival, comparative statics of \(\kappa^*\) in \(\delta_3\) are most transparent in a

two-product reduction (firms 1 and 3 only).

Proposition 2. In a two-product reduction

(eliminate firm 2 and product 2), the comparative static \(d\kappa^*/d\delta_3\) has no fixed sign:

depending on the remaining primitives, the indifference cutoff \(\kappa^*(\delta_3)\) can rise or fall as

the foreign product becomes more attractive.

As \(\delta_3\) rises, the foreign

product becomes more appealing. The relative effect on firm 1’s profits

differs by regime. Under petitioning, the tariff has two opposing

effects: by handicapping the foreign rival it shrinks the rival’s share

and insulates firm 1, but by making firm 1 the dominant domestic

producer it widens firm 1’s markup and leaves more profit exposed to a

more appealing rival. When the duty is large enough to nearly eliminate

the rival, the first effect dominates and petitioning insulates firm 1

more than offshoring, so \(\kappa^*(\delta_3)\) falls; when the

foreign rival remains strong even under the duty, the second effect

dominates and offshoring insulates more, so \(\kappa^*(\delta_3)\)

rises.This

is not true for any demand system. Under CES demand with monopolistic

competition (where each firm takes the price index as given), markups

are constant and the price of firm 1 does not react to the quality of

product 3. In a finite-firm CES oligopoly, markups depend on market

shares and some strategic interaction is restored, but it remains weaker

than under logit demand.

I first compare firm 1’s gain from petitioning for a given \(\kappa\), with and without the merger,

against a status-quo baseline.

Proposition 3. Let \[\begin{equation}

\tag{6}

\Delta^{\text{pet}}_{1,\mathcal{M}}\;\equiv\;\Pi^{\text{pet}}_{\mathcal{M}}\;-\;\Pi^{\text{sq}}_{\mathcal{M}},

\qquad

\Delta^{\text{pet}}_{1,\mathcal{S}}\;\equiv\;\Pi^{\text{pet}}_{1,\mathcal{S}}\;-\;\Pi^{\text{sq}}_{1,\mathcal{S}},

\label{eq:premium_sq}

\end{equation}\] be firm 1’s petitioning premium with and without

the merger. Then the merger’s impact admits the exact decomposition

\[\begin{equation}

\tag{7}

\Delta^{\text{pet}}_{1,\mathcal{M}}-\Delta^{\text{pet}}_{1,\mathcal{S}}

=\underbrace{\big(\pi^{\text{pet}}_{2,\mathcal{S}}-\pi^{\text{sq}}_{2,\mathcal{S}}\big)}_{\text{\emph{appropriation}}}

+\underbrace{\Big[(\pi^{\text{pet}}_{\mathcal{M}}-\pi^{\text{sq}}_{\mathcal{M}})

-(\pi^{\text{pet}}_{1,\mathcal{S}}+\pi^{\text{pet}}_{2,\mathcal{S}}-\pi^{\text{sq}}_{1,\mathcal{S}}-\pi^{\text{sq}}_{2,\mathcal{S}})\Big]}_{\text{\emph{strategic}}}.

\label{eq:decomp_sq}

\end{equation}\] Both the appropriation and the strategic effect

are strictly positive, so the merger strictly increases firm 1’s gains

from tariffs.

The appropriation effect captures the fact that the merger

internalizes a petitioning externality: firm 1 can now appropriate the

rents from tariff protection that would otherwise accrue to firm 2. The

strategic effect captures the fact that the merger raises how much firms

1 and 2 jointly gain from tariffs. Intuitively, the merged firm has

already internalized domestic competition, so the foreign rival

constitutes a proportionally larger part of its competitive environment;

weakening the foreign firm via the tariff therefore benefits the merged

entity more than the standalone firms. The aggregative-games framework

of Nocke and

Schutz (2018, 2025) underpins this result.

While I rely on logit demand, the result that the merger increases

firm 1’s gains from tariffs is true under mild assumptions on demand

(downward-sloping demand, substitutability across products, and standard

regularity conditions). In particular, while the strategic effect is

zero under CES demand with monopolistic competition, the appropriation

effect, and thus the overall effect, remain positive.

Next, I switch the baseline from status quo to offshoring.

Proposition 4. Let \[\begin{equation}

\tag{8}

\Delta^{\text{pet}}_{1,\mathcal{M}}\;\equiv\;\Pi^{\text{pet}}_{\mathcal{M}}\;-\;\Pi^{\text{off}}_{\mathcal{M}},

\qquad

\Delta^{\text{pet}}_{1,\mathcal{S}}\;\equiv\;\Pi^{\text{pet}}_{1,\mathcal{S}}\;-\;\Pi^{\text{off}}_{1,\mathcal{S}},

\label{eq:premium_off}

\end{equation}\] be firm 1’s petitioning premium with and without

the merger. Then the merger’s impact admits the exact decomposition

\[\begin{equation}

\tag{9}

\Delta^{\text{pet}}_{1,\mathcal{M}}-\Delta^{\text{pet}}_{1,\mathcal{S}}

=\underbrace{\big(\pi^{\text{pet}}_{2,\mathcal{S}}-\pi^{\text{off}}_{2,\mathcal{S}}\big)}_{\text{\emph{appropriation}}}

+\underbrace{\Big[(\pi^{\text{pet}}_{\mathcal{M}}-\pi^{\text{off}}_{\mathcal{M}})

-(\pi^{\text{pet}}_{1,\mathcal{S}}+\pi^{\text{pet}}_{2,\mathcal{S}}-\pi^{\text{off}}_{1,\mathcal{S}}-\pi^{\text{off}}_{2,\mathcal{S}})\Big]}_{\text{\emph{strategic}}}.

\label{eq:decomp_off}

\end{equation}\] The appropriation effect is strictly positive.

The strategic effect is strictly increasing in \(\kappa\), and there is a unique threshold

\(\kappa^{SE}\in[0,\infty]\) such that

it is positive if and only if \(\kappa>\kappa^{SE}\). The threshold is

strictly positive whenever the merger raises the joint gains from

offshoring, and it is infinite when the merger’s excess offshoring gain

exceeds its gain from a prohibitive tariff.

The strategic effect reflects two competing forces. First, by

Proposition 3, the tariff raises the merged

entity’s profit by strictly more than the sum of standalone profits. So

the tariff gain is larger with the merger, and increasingly so

as \(\kappa\) rises. Second, offshoring

lowers costs, and the merger uniquely enables offshoring of product 2.

So the offshoring gain is also larger with the merger,

independently of \(\kappa\). The

strategic effect is the difference between these two forces. When the

cost gap \(c_D - c_F\) is small, the

threshold \(\kappa^{SE}\) is low and

even moderate tariffs make the strategic effect positive. When the

offshoring option is sufficiently valuable, the tariff gain falls short

at every duty level and the strategic effect is negative throughout:

protection, however high, cannot compensate the merged firm for the cost

savings it forgoes.

Even if a merger makes petitioning relatively more attractive (i.e.,

decreases \(\kappa^*\)), firm 1 will

not petition for tariffs if the tariff rate \(\kappa\) that the trade commission sets in

the event of a petition is below the post-merger \(\kappa^*\).

Finally, I consider how the consumer harm from a given tariff changes

with a domestic merger.

Proposition 5. A domestic merger raises the

consumer harm from a given tariff \(\kappa\).

The marginal consumer harm from the tariff is affected by the merger

through two channels. The merger raises the foreign share \(s_3\) (higher domestic prices shift demand

to the foreign product). The merger also concentrates domestic

production into a single firm. Pooling the domestic firms into one

raises the strategic-complementarity multiplier that grows with each

firm’s market share. The merger increases consumer harm regardless of

\(s_3\).

Foreign-rival

response in a two-period model

To assess the robustness of these results, I consider a two-period

extension in which firm 3 can respond to the tariff by relocating

production to the domestic market. Firm 1 maximizes the discounted sum

of profits \(\Pi_{1} = \Pi_1^{t=1} + \beta

\Pi_1^{t=2}\), where \(\beta \in

[0,1]\).

In the first period, marginal costs are determined as in the static

model. In the second period, if a tariff is in place, firm 3 may choose

to pay a fixed cost \(R_3\) to

relocate. A necessary condition for firm 3 to relocate to \(D\) is that the tariff is high enough that

\(c_D < (1+\kappa) c_F\). I focus on

the case where \(R_3\) is small enough

that tariff jumping is firm 3’s best response.

Tariff jumping strictly reduces the incentive to petition relative to

offshoring: it erodes the future rents from protection while leaving the

offshoring payoff unchanged. However, petitioning can remain optimal

even with perfect patience (\(\beta =

1\)) and certainty of tariff jumping in \(t=2\), provided the short-run windfall from

the tariff is sufficiently large. The appropriation and strategic

effects from Propositions 3

and 4 operate in full during

the period of tariff protection.

In the second period, the comparison across merger regimes is more

complex: tariff jumping equalizes the foreign rival’s costs, but the

merger also changes the offshoring counterfactual by enabling relocation

of product 2 and alters equilibrium pricing through joint ownership. The

net second-period effect is parameter-dependent, but the first-period

mechanism through which the merger increases the incentive to petition

remains intact.

Cross-border mergers

The previous results highlighted how a merger between domestic

producers can create demand for protectionist policies and magnify their

harm to consumers. A natural question is whether cross-border mergers

generate the same forces.

To analyze this, I extend the setup to four firms. Firm 4 is a second

foreign producer with marginal cost \(c_F\), acquired by firm 1 in a cross-border

merger \(\mathcal{X} = \{1,4\}\). Firms

2 and 3 remain independent. I impose the following institutional

constraint: if the merged entity petitions for tariffs on foreign

imports, it must relocate product 4’s production from \(F\) to \(D\) at cost \(R_1\), raising its marginal cost from \(c_F\) to \(c_D\). The rationale is that a firm cannot

credibly petition for duties on foreign-produced goods while itself

importing the same goods, since AD/CVD standing requires the petitioner

to represent domestic production. Offshoring remains available only for

product 1 (product 4 is already produced abroad), again at cost \(R_1\).

Proposition 6. Let \[\begin{equation}

\tag{10}

\Delta^{\text{pet}}_{1,\mathcal{X}}\;\equiv\;\Pi^{\text{pet}}_{\mathcal{X}}\;-\;\Pi^{\text{sq}}_{\mathcal{X}},

\qquad

\Delta^{\text{pet}}_{1,\mathcal{S}}\;\equiv\;\Pi^{\text{pet}}_{1,\mathcal{S}}\;-\;\Pi^{\text{sq}}_{1,\mathcal{S}},

\label{eq:premium_xb}

\end{equation}\] be firm 1’s petitioning premium (relative to

status quo) with and without the cross-border merger, where \(\Pi^{\text{pet}}_{\mathcal{X}} =

\pi^{\text{pet}}_{\mathcal{X}} - L - R_1\) includes both

petitioning costs and the cost of relocating product 4. Then the

merger’s impact admits the exact decomposition \[\begin{equation}

\tag{11}

\Delta^{\text{pet}}_{1,\mathcal{X}}-\Delta^{\text{pet}}_{1,\mathcal{S}}

=\underbrace{\big(\pi^{\text{pet}}_{4,\mathcal{S}}-\pi^{\text{sq}}_{4,\mathcal{S}}\big)}_{\text{\emph{appropriation}}}

+\underbrace{\Big[(\pi^{\text{pet}}_{\mathcal{X}}-\pi^{\text{sq}}_{\mathcal{X}})

-(\pi^{\text{pet}}_{1,\mathcal{S}}+\pi^{\text{pet}}_{4,\mathcal{S}}-\pi^{\text{sq}}_{1,\mathcal{S}}-\pi^{\text{sq}}_{4,\mathcal{S}})\Big]}_{\text{\emph{strategic}}}

-\underbrace{R_1}_{\text{\emph{relocation cost}}}.

\label{eq:decomp_xb}

\end{equation}\] The appropriation effect is strictly negative;

the relocation cost is strictly positive; and the strategic effect can

take either sign.

The contrast with the domestic merger under the status quo baseline

(Proposition 3) is stark. In the domestic

case, both the appropriation and strategic effects are strictly

positive. The merger internalizes a positive externality, since the

domestic target benefits from the tariff. In the cross-border case, the

target is a victim of the tariff. Internalizing its profit change means

internalizing a loss. The appropriation effect flips sign, and the

merged entity must additionally bear the relocation cost \(R_1\) to petition credibly. The strategic

effect in the cross-border case conflates two channels — joint pricing

under the merger and the variable cost restructuring from relocating

product 4 — so it does not isolate the pure joint-pricing surplus as in

Proposition 3, and its sign can go either

way.

When the baseline is offshoring instead of status quo, the same

decomposition structure applies. The appropriation term becomes \(\pi^{\text{pet}}_{4,\mathcal{S}} -

\pi^{\text{off}}_{4,\mathcal{S}}\), which is ambiguous in sign:

when \(\kappa\) is small, firm 4 may

prefer the petitioning world (firm 1 remains a weak competitor at \(c_D\)); when \(\kappa\) is large, the direct cost penalty

on firm 4 dominates. The strategic effect is also ambiguous in sign, and

the relocation cost \(R_1\) is still

strictly positive. By contrast, in the domestic merger (Proposition 4), the appropriation

effect is strictly positive.

While the overall effect of a cross-border merger on petitioning

incentives remains parameter-dependent, the decompositions suggest that

cross-border mergers are less likely to increase the demand for

protectionism. I quantify these channels for a specific empirical

application in Section 7.

Institutional Setting, Data, and Descriptive

Evidence

To study the interplay between mergers, concentration, and the demand

for trade protection in a concrete setting, and to illustrate how the

trade-policy channel of mergers could be incorporated into merger

policy, I focus on the household appliance industry.

Household Appliance Industry

In 2000, the import share for most major appliances in the EU and

U.S. was below 10 percent. By 2018, it exceeded 30 percent for most

categories and approached 50 percent for some, such as clothes washers,

dryers, and refrigerators.

European manufacturers such as BSH and Electrolux had established a

presence in the U.S. by the 1990s, and U.S. firms such as Whirlpool were

similarly active in Europe. However, these firms produced locally rather

than exporting across regions. The U.S. market saw new entry from LG and

Samsung in the mid-2000s, and from Haier, which first attempted to

acquire Maytag in 2005 and later entered successfully by acquiring GE

Appliances in 2016. European markets experienced a similar pattern, with

entry from Arçelik and Vestel (Turkey), followed by LG and Samsung

(Korea), and later Haier and Hisense (China).

In 2006, Whirlpool, the leading U.S. appliance manufacturer, acquired

Maytag, its main domestically producing rival. The Department of Justice

cleared the merger on the grounds that foreign manufacturers posed a

sufficiently large competitive constraint to prevent post-merger price

increases (Department of

Justice 2006).

The rise in import share reflects both foreign entrants producing

abroad and domestic incumbents shifting production overseas. Some

incumbents offshore part of their previously domestic output; others

relocate all of it.

Although product market concentration increased modestly across most

markets, the key variation between markets lies in the decline of major

domestic producers. By 2015, the U.S. market for clothes washers and

bottom-mount refrigerators had only two domestic producers remaining,

compared to at least four for EU washers and U.S. dishwashers. The

markets with few domestic producers are also those where Whirlpool filed

for AD/CVD.

While the U.S. petition for bottom-mount refrigerators was ultimately

unsuccessful,See

U.S. International Trade Commission, Investigation Nos. 701-TA-477 and

731-TA-1180-1181, 2012. large residential washers (LRWs) were

subject to multiple rounds of tariffs. Preliminary antidumping duties

were first imposed on imports from Korea and Mexico in 2012, followed by

antidumping duties on washers produced in China in 2016, and culminating

in a global safeguard in 2018 (Flaaen et al. 2020).

Data

The primary data source is the TraQline household survey, described

in detail in Montag

(2026). TraQline surveys approximately 600,000 U.S. households

annually on major appliance purchases, including product

characteristics, prices, second-choice brands, the retailer, and

household demographics. I observe survey responses for 2005–2015. The

product scope includes refrigerators, dishwashers, clothes washers,

dryers, and freestanding ranges. I define products as

brand-retailer-characteristic combinations, using brand identity and

retailer as proxies for unobserved differentiation. I define a market as

a product category in a given country or region, for example U.S.

clothes washers.

For the descriptive analysis, I extend the market share series

through 2023, using OpenBrand data provided by Dewey Data (OpenBrand

2022).TraQline

has been part of OpenBrand since 2024. This extended dataset does

not include non-price product characteristics other than brand, so the

structural analysis cannot be extended beyond 2015.

To measure product market concentration in the European washer

industry, I use washing machine sales for most European countries

between 2000 and 2018 from Gesellschaft für

Konsumforschung.

To measure the number of major domestic producers by market and year,

I combine production data from Appliance Magazine, Euromonitor, and

hand-collected information on production locations for the years 2000

through 2023, subject to availability. For U.S. clothes washers in

2005–2015, I use hand-collected production location data from Montag (2026).

Finally, I compute import shares for each market and year using trade

data from the USITC and COMTRADE.

Descriptive analysis

The stylized model in Section 3 suggests

that mergers between domestic producers are particularly likely to

generate demand for trade protection, implying that petitions should be

more common in markets with few domestic producers.

To examine which market characteristics are associated with domestic

producers petitioning for trade protection, I estimate a linear

probability model at the market-year level for the household appliance

industry. The dependent variable is an indicator for whether a petition

for AD/CVD or global safeguards was filed in a given market and year.

Whirlpool filed AD/CVD petitions on bottom-mount refrigerator imports

into the U.S. from Korea and Mexico on March 30, 2011 and on large

residential washers into the U.S. from Korea and Mexico on December 30,

2011.The

results are insensitive to moving the filing date of the washer petition

from 2011 to 2012. The analysis is descriptive and does not claim

to identify causal effects.

The linear probability model relates petition incidence to three key

market-level variables: the import share, the degree of domestic product

market concentration, and the number of domestic producers. I estimate

the parameters of the following specification: \[\begin{equation}

\tag{12}

\mathbb{1}\{ \text{Petition}_{it} \} = \beta_1 \, \text{impshare}_{it} +

\beta_2 \, \text{prodmkthhi}_{it} + \beta_3 \, \text{domprod}_{it} +

\delta_i + \gamma_t + \varepsilon_{it},

\label{eq:lpm}

\end{equation}\] where \(i\)

indexes product markets and \(t\)

denotes years. The model includes market fixed effects \(\delta_i\) and year fixed effects \(\gamma_t\).

The outcome \(\mathbb{1}\{

\text{Petition}_{it} \}\) is an indicator for whether a trade

remedy petition was filed in market \(i\) in year \(t\). The variable \(\text{impshare}_{it}\) measures the import

share in the market, \(\text{prodmkthhi}_{it}\) is the

Herfindahl-Hirschman Index based on each producer’s (foreign and

domestic) sales share in the domestic market, and \(\text{domprod}_{it}\) is the number of

domestic producers or an indicator equal to one if there are more than

two domestic producers.

The data span the years 2000 through 2023 and include five product

markets: U.S. clothes washers, U.S. clothes dryers, U.S. dishwashers,

U.S. bottom-mount refrigerators, and EU clothes washers. Each of these

markets is observed at annual frequency; however, data are not available

for all product markets in all years, resulting in an unbalanced

panel.

Table 1: Descriptive correlates of trade

remedy petitions

(1)

(2)

(3)

(4)

(5)

(6)

Import share

0.90\(^{***}\)

0.98\(^{***}\)

0.26

\(-\)0.35\(^{*}\)

0.06

\(-\)1.14

(0.23)

(0.35)

(1.46)

(0.19)

(0.14)

(1.20)

Market HHI

\(-\)2.14

\(-\)4.81\(^{***}\)

\(-\)6.41\(^{**}\)

0.35

\(-\)1.55

0.57

(1.31)

(1.79)

(2.44)

(0.35)

(1.35)

(1.76)

# of domestic producers

\(-\)0.05\(^{***}\)

\(-\)0.14\(^{***}\)

\(-\)0.24\(^{***}\)

(0.01)

(0.03)

(0.05)

\(\mathbb{1}\{\text{\# dom. prod.} >

2\}\)

\(-\)0.86\(^{***}\)

\(-\)0.81\(^{***}\)

\(-\)0.80\(^{***}\)

(0.08)

(0.10)

(0.11)

Market FE

No

Yes

Yes

No

Yes

Yes

Year FE

No

No

Yes

No

No

Yes

Observations

72

72

72

72

72

72

Notes: Each column reports coefficients from a linear

probability model at the market-year level. The outcome is an indicator

for whether a trade remedy petition was filed. Heteroskedasticity-robust

standard errors in parentheses. \(^{*}\)\(p<0.10\), \(^{**}\)\(p<0.05\), \(^{***}\)\(p<0.01\).

The descriptive estimates of equation (12) in

Table 1 indicate that higher

product market concentration, as measured by the HHI, is not positively

associated with petition filing. If anything, the association is

negative or indistinguishable from zero. In contrast, the number of

domestic producers is strongly and negatively associated with the

likelihood of a petition. In particular, markets with two or fewer

domestic producers are substantially more likely to see a filing. This

pattern may reflect that petitions typically arise only after most

domestic competitors have already exited. Alternatively, it may indicate

that petitioners expect greater benefit from trade protection when fewer

domestic firms remain to share the resulting market expansion. The

following sections evaluate this second channel quantitatively in the

case of the U.S. clothes washer market.

Empirical Model and Estimation

The stylized model in Section 3 showed

that assessing whether a merger harms consumers through the trade-policy

channel requires estimating the merging parties’ variable profits under

different merger, tariff, and production-location scenarios. To estimate

these objects, I specify a model of demand and supply tailored to the

U.S. washer

market.The

empirical model closely follows Montag (2026).

Consumer Demand

Let utility for household \(i\) from

purchasing product \(j\) be: \[\begin{equation}

\tag{13}

u_{ijt} \;=\; x_{jt}\beta \;+\; \sigma^{\text{FL}} \nu_i^{\text{FL}}

x_{jt}^{\text{FL}} \;-\; \alpha_i\, p_{jt} \;+\; \xi_{jt} \;+\;

\varepsilon_{ijt},

\qquad

\alpha_i \equiv \exp(\alpha + \kappa_\alpha \iota_i),

\label{eq:emp_utility}

\end{equation}\] where \(x_{jt}\) is a vector of observed non-price

characteristics, \(x_{jt}^{\text{FL}}\)

is a front-loader indicator, \(\nu_i^{\text{FL}} \sim \mathcal{N}(0,1)\)

is a random taste draw that captures heterogeneous preferences for

front-loaders, \(\iota_i\) is income,

and \(\varepsilon_{ijt}\) is an

idiosyncratic shock drawn from a Type I extreme value distribution.

The utility of the outside good is normalized to zero. Each consumer

purchases the single product, or the outside good, that yields the

highest utility.

Given the distributional assumptions, the market share of product

\(j\) is \[\begin{equation}

\tag{14}

s_{jt}(\mathbf p)

\;=\;

\int

\frac{\exp\!\big(\delta_{jt} + \mu_{ijt}\big)}

{\,1 + \sum_{k \in J} \exp\!\big(\delta_{kt} + \mu_{ikt}\big)}

\, dP(\iota_i,\nu_i),

\label{eq:emp_share}

\end{equation}\] where \[\delta_{jt}=x_{jt}\beta+\xi_{jt},

\qquad

\mu_{ijt}=\sigma^{\text{FL}} \nu_i^{\text{FL}}

x_{jt}^{\text{FL}}-\alpha_i p_{jt}.\]

Demand is estimated by combining aggregate and household moments as

outlined in Berry et al.

(2004). I split the demand parameters into a linear component

\(\theta_1\), the coefficients \(\beta\) on product characteristics, and a

nonlinear component \(\theta_2 =

(\sigma^{\text{FL}}, \alpha, \kappa_\alpha)\). The nonlinear

parameters are estimated by the method of simulated moments using three

moment conditions: two match household-level moments between the

simulated and observed data, and the third is the orthogonality

condition implied by excluding the real exchange rate, a cost shifter,

from utility. With as many moments as parameters, \(\theta_2\) is exactly identified.

Conditional on the estimate \(\hat\theta_2\), the linear parameters \(\theta_1\) are obtained by ordinary least

squares. The data, estimation procedure, and moment conditions are the

same as in Montag

(2026). I refer readers to that paper for further details.

Marginal Costs and Pricing

Let \(j \in J_{ft}\) denote a

product offered by firm \(f\) in market

\(t\) with price \(p_{jt}\) and marginal cost \(mc_{jt}\). The firm’s variable profit is:

\[\begin{equation}

\tag{15}

\pi_{ft} = \sum_{j \in J_{ft}} (p_{jt} - mc_{jt}) \cdot

s_{jt}(\mathbf{p}) \cdot M_t,

\label{eq:emp_profit}

\end{equation}\] where \(s_{jt}(\mathbf{p})\) is the market share of

product \(j\) as a function of all

prices \(\mathbf{p}\), and \(M_t\) is market size.

Markups are pinned down by the derivatives of market shares with

respect to prices. The Bertrand-Nash equilibrium prices solve: \[\begin{equation}

\tag{16}

\mathbf{p} = \mathbf{mc} - \left( \frac{\partial \mathbf{s}}{\partial

\mathbf{p}} \circ \Omega \right)^{-1} \mathbf{s},

\label{eq:emp_pricing}

\end{equation}\] where \(\Omega\) is the ownership matrix and \(\circ\) denotes the Hadamard product.

Let \(c(j)\) denote the country of

origin of product \(j\); baseline

(tariff-exclusive) marginal cost is \[\begin{equation}

\tag{17}

mc_{jt} \;=\; \lambda_{1f(j)} r_{f(j)t} \;+\; \lambda_2 w_{c(j)t} \;+\;

\lambda_{3j} m_t \;+\; \omega_{jt},

\label{eq:mc}

\end{equation}\] where \(r_{f(j)t}\), \(w_{c(j)t}\), and \(m_t\) are input prices for capital, labor,

and materials; and \(\omega_{jt}\) is a

product-level marginal-cost shock realized after production and sourcing

decisions. Offshoring modifies \(c(j)\)

and thus affects the labor-cost component.

Alternatively, the incumbent may petition for an ad valorem tariff

\(\kappa>0\) on imports from an

origin set \(O\). Tariff-origin pairs

are indexed by \((\kappa,O)\).I

assume that petitions always lead to tariffs. This does not affect the

sign of the comparison between merger and no-merger petitioning

incentives: a common petition success probability \(\rho<1\) multiplies each firm’s expected

petitioning premium by \(\rho\), while

the filing cost \(L\) cancels in the

merger-vs-no-merger difference. The decomposition into appropriation and

strategic effects is therefore preserved, with both terms scaled by

\(\rho\). Tariffs modify

marginal costs multiplicatively: \[\begin{equation}

\tag{18}

mc_{jt}^{(\kappa,O)} \;=\; \bigl[1 + \kappa \cdot \mathbb{1}\{c(j)\in

O\}\bigr]\; mc_{jt}.

\label{eq:mc_tariff}

\end{equation}\]

Marginal costs are recovered by inverting firms’ first-order pricing

conditions using observed market shares and prices. To estimate how

marginal costs change with input costs, I estimate: \[\begin{equation}

\tag{19}

\displaystyle mc_{jt} = FE_f + \gamma_1 RER_{c(j)t} + \gamma_2 x_{j}

+\omega_{jt} \,.

\label{eq:mc_reg}

\end{equation}\]

Firm fixed effects \(FE_f\) capture

differences in capital intensity across firms. The real exchange rate

\(RER_{c(j)t}\) is a product-level cost

shifter capturing local wage and nominal exchange rate fluctuations. The

non-price characteristics \(x_j\)

capture material cost differences across products, while \(\omega_{jt}\) denotes transitory

marginal-cost shocks.

Trade-Policy Channel of

Mergers

With the tools to estimate firm profits under different merger,

offshoring, and tariff scenarios, I can now connect the empirical model

to the propositions in Section 3. The model

shows that assessing how a merger changes the merging parties’

incentives to petition for tariffs requires estimating the

appropriation and strategic effects in equations (7) and (9).

Let \(\pi_{f,t,\mathcal{S}}(\kappa,O;\ell)\)

denote the variable profits of firm \(f\) in year \(t\) under separate ownership (\(\mathcal{S}\)), and \(\pi_{t,\mathcal{M}}(\kappa,O;\ell)\) the

variable profits of the merged entity (\(\mathcal{M}\)), which owns both merging

firms’ products. Profits are evaluated at tariff-origin pair \((\kappa,O)\) and pre-petition

production-location regime \(\ell\in\{\text{off},\text{sq},\text{dom}\}\)

(offshore, status quo, domestic). When evaluating profits under a tariff

petition, I take the with-tariff regime for the incumbent to be domestic

production, i.e., \(\ell=\text{dom}\).

For simplicity, in the remainder I denote the acquirer as \(f=1\) and the acquisition target as \(f=2\).

Then the appropriation effect of a merger can be written as \[\begin{equation}

\tag{20}

\text{Appropriation}_t(\kappa, O, \ell) =

\pi_{2,t,\mathcal{S}}(\kappa,O;\text{dom}) -

\pi_{2,t,\mathcal{S}}(0,O;\ell)

\label{eq:emp_appropriation}

\end{equation}\]

and the strategic effect can be written as \[\begin{equation}

\tag{21}

\begin{split}

\text{Strategic}_t(\kappa, O, \ell) = \Bigl[ &

\pi_{t,\mathcal{M}}(\kappa,O;\text{dom}) -

\pi_{1,t,\mathcal{S}}(\kappa,O;\text{dom}) -

\pi_{2,t,\mathcal{S}}(\kappa,O;\text{dom})\Bigr] \\

-\; \Bigl[ & \pi_{t,\mathcal{M}}(0,O;\ell) -

\pi_{1,t,\mathcal{S}}(0,O;\ell) - \pi_{2,t,\mathcal{S}}(0,O;\ell)\Bigr]

\,.

\end{split}

\label{eq:emp_strategic}

\end{equation}\]

Finally, I quantify the consumer-surplus effect of a given tariff.

For a tariff-origin pair \((\kappa,O)\), the change in consumer

surplus under ownership structure \(m\in\{\mathcal M,\mathcal S\}\) is (Small and Rosen 1981)\[\begin{equation}

\tag{22}

CS^{m}(\kappa,O)

\;=\;

\int \frac{1}{\alpha_i}

\Bigg[

\ln\!\Big(\sum_{j=0}^J e^{V_{ij}^{(\kappa,O;\,m)}}\Big)

-\ln\!\Big(\sum_{j=0}^J e^{V_{ij}^{(0,O;\,m)}}\Big)

\Bigg]\,

dP(\iota_i,\nu_i),

\label{eq:emp_cs}

\end{equation}\] where \(V_{ij}^{(\kappa,O;\,m)}=\delta_{jt}+\mu_{ijt}^{(\kappa,O;\,m)}\)

uses the equilibrium prices implied by \(m\) and \((\kappa,O)\).

For a given tariff-origin pair \((\kappa,O)\), the merger-induced change in

consumer surplus from a tariff is \[\begin{equation}

\tag{23}

\Delta CS^{\mathcal M}(\kappa,O)

\;:=\;

CS^{\mathcal M}(\kappa,O)\;-\;CS^{\mathcal S}(\kappa,O),

\label{eq:emp_dcs}

\end{equation}\] so \(\Delta

CS^{\mathcal M}(\kappa,O)<0\) indicates that the merger

amplifies the consumer harm from a tariff.

Parameter Estimates

Table 2 summarizes the demand estimates.

Column (1) shows that the real exchange rate is a strong instrument for

price. The estimates in Column (4) imply that higher-income households

are less price-sensitive (the income coefficient \(\kappa_\alpha\) is negative) and that

households differ in their taste for front-loaders (the unobserved-taste

dispersion \(\sigma^{\text{FL}}\) is

positive and significant). The average own-price elasticity in the full

mixed-logit model is \(-2.54\) at the

product level.

Table 2: Demand estimates

(1)

(2)

(3)

(4)

First stage

Logit OLS

Logit IV

Mixed logit

Dependent variable:

Price

\(\hat{\delta}_{jt}\)

\(\hat{\delta}_{jt}\)

Linear parameters

Real exchange rate

2.033\(^{***}\)

(0.365)

Price (’00 2012 $)

\(-\)0.164\(^{***}\)

\(-\)0.351\(^{**}\)

(0.062)

(0.178)

Nonlinear parameters

Common price coefficient \(\alpha\)

\(-\)0.675\(^{***}\)

(0.033)

Income effect \(\kappa_{\alpha}\)

\(-\)0.210\(^{***}\)

(0.024)

Unobserved taste \(\sigma^{\text{FL}}\)

2.493\(^{***}\)

(0.068)

Characteristics

Yes

Yes

Yes

Yes

Retailer FE

Yes

Yes

Yes

Yes

Brand FE

Yes

Yes

Yes

Yes

Brand time trends

Yes

Yes

Yes

Yes

Year FE

Yes

Yes

Yes

Yes

Observations

1,590

1,586

1,590

1,590

Kleibergen–Paap F-statistic

31.041

Avg. own-price elasticity

\(-\)0.964

\(-\)2.058

\(-\)2.542

Notes: Column (1) reports the first-stage regression results

of prices on the real exchange rate. Column (2) presents estimates from

the simple logit model without instrumentation. Column (3) shows

estimates from the simple logit using the RER as an instrument for

price. Column (4) displays results from the mixed logit model described

in Section 5. Standard errors are clustered at the

brand level. Own-price elasticities of residual demand are computed at

the product level and averaged across products, weighting by sales

volume. Significance levels: \(^{*}\)\(p<0.10\), \(^{**}\)\(p<0.05\), \(^{***}\)\(p<0.01\).

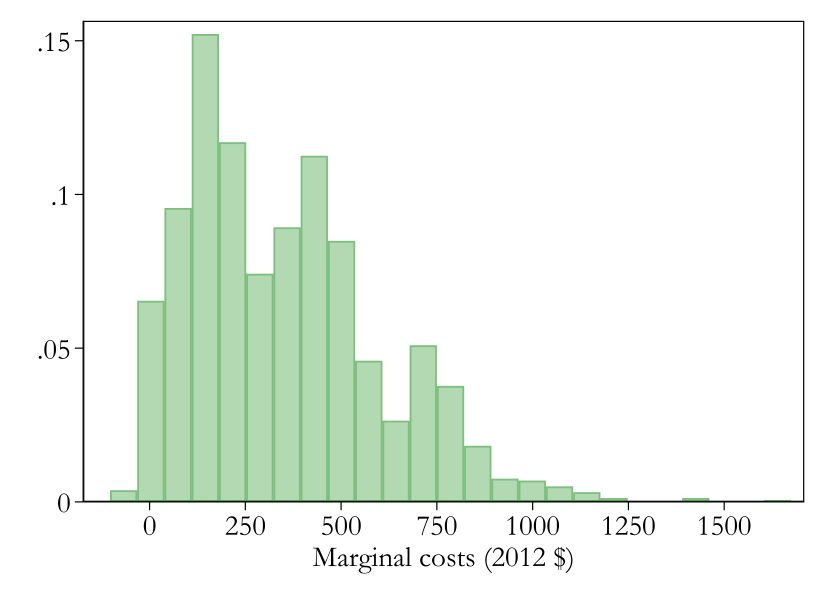

Figure 2 displays the distribution of

estimated marginal costs across all products.

Notes: Histogram of estimated marginal costs (deflated to

2012 dollars) across all products in the sample.

Figure 2: Histogram of product-level

marginal cost estimates

Finally, Table 3 quantifies how marginal costs

depend on labor costs (captured by the deflated RER), product

characteristics, and brand, retailer, and year fixed effects. As labor

costs increase, the estimated marginal cost increases. Furthermore,

top-loaders with an agitator have lower marginal costs than

high-efficiency top-loaders and front-loaders.

Table 3: Marginal cost decomposition

Marginal costs (2012

$)

Real Exchange Rate

199.324\(^{***}\)

(36.869)

Front-Loader

21.042

(20.161)

Agitator

\(-\)244.397\(^{***}\)

(26.696)

Characteristics

Yes

Retailer FE

Yes

Brand FE

Yes

Brand time trends

Yes

Year FE

Yes

N

1,586

Notes: The table presents regression results of

product-level marginal costs on proxies for labor and shipping costs,

product characteristics, fixed effects, and brand-specific time trends.

Standard errors are clustered at the brand level. Significance levels:

\(^{*}\)\(p<0.10\), \(^{**}\)\(p<0.05\), \(^{***}\)\(p<0.01\).

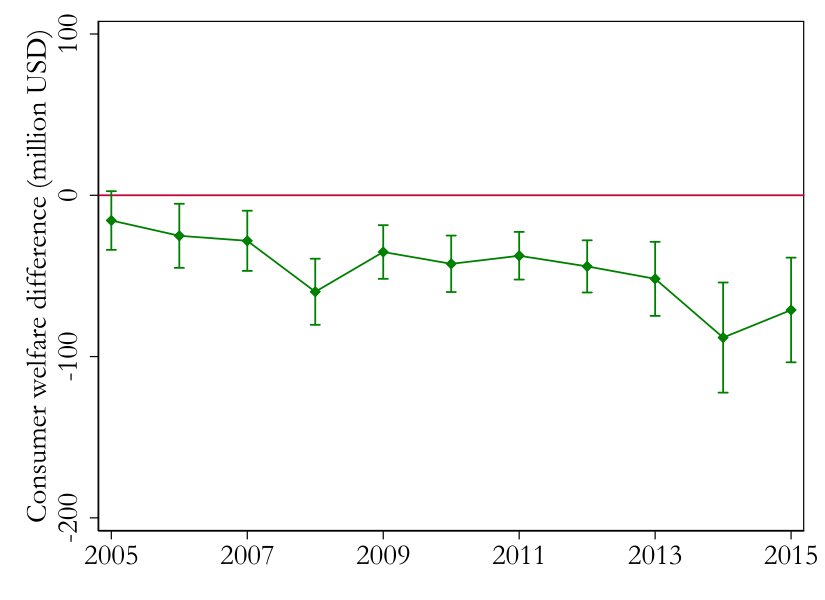

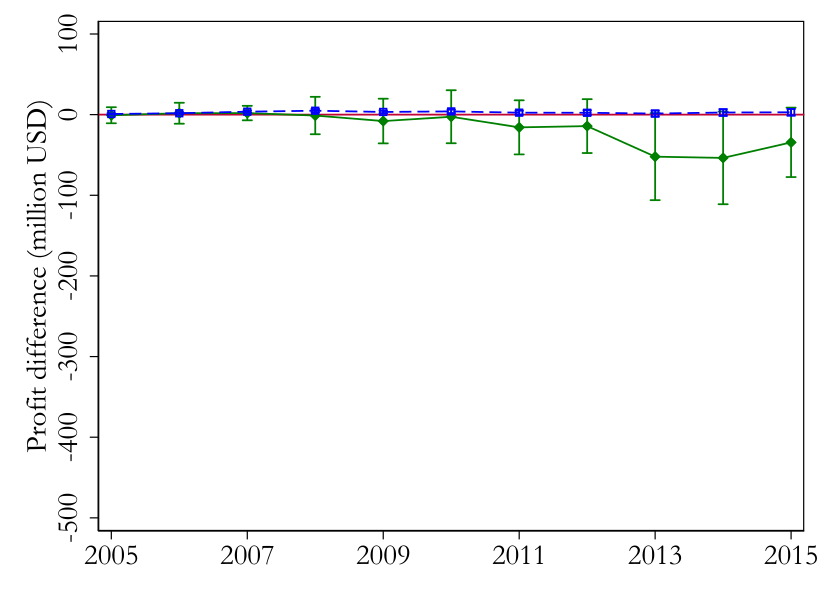

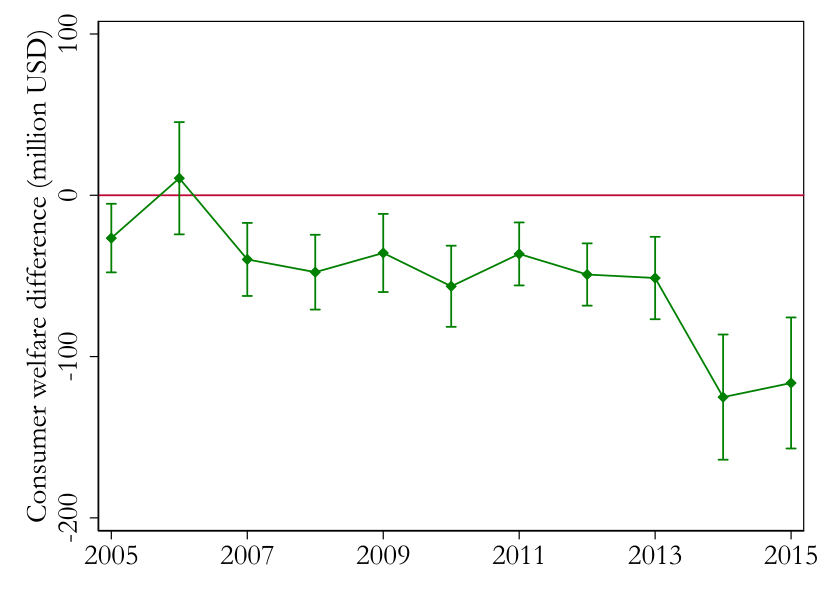

Quantifying the Trade-Policy Channel for

Whirlpool

In this section, I quantify the components of the trade-policy

channel for Whirlpool’s domestic acquisition of Maytag, assessing how

the merger affected the profitability of petitioning across the

different rounds of tariff actions observed between 2011 and 2018. To

contrast this with the trade-policy channel of a cross-border merger, I

perform the same analysis for a hypothetical merger between Whirlpool

and LG.

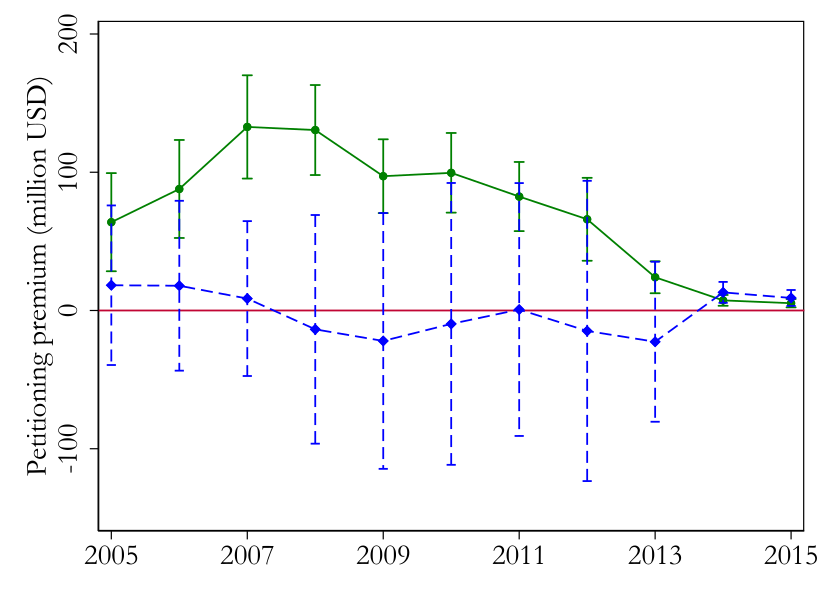

Trade-Policy Channel

of a Domestic Merger

To assess how acquiring Maytag affected Whirlpool’s incentives to

petition for tariffs, I quantify the appropriation and strategic effects

(equations (20) and (21)) for different

tariff-origin scenarios. I also estimate the corresponding consumer

surplus effect \(\Delta CS^{\mathcal

M}(\kappa,O)\) defined in equation (23).

While I observe realized tariff outcomes and relocation responses by

LG and Samsung, the simulations do not incorporate this ex post

information. Ex ante, petitioners cannot perfectly predict final tariffs

or rivals’ immediate relocation strategies; for instance, preliminary AD

margins on LRW imports from China were substantially revised downward

between preliminary and final determinations (LG: \(49.88\%\rightarrow 32.12\%\); Samsung:

\(111.09\%\rightarrow 52.51\%\)). I

instead simulate uniform ad valorem tariffs of \(\kappa=50\%\) applied to three origin

groups, \[O \in \{\text{Korea+Mexico},\

\text{China+Korea+Mexico},\ \text{Global}\},\] which mirror the

historical sequence (2011 Korea and Mexico; 2015 China; 2018 global

safeguards).AD/CVD

petitions on imports from Korea and Mexico, as well as China, were filed

in 2011 and 2015, respectively. Final duty determinations were made in

2013 and 2016, respectively.

For each calendar year \(t\), I

recompute the Bertrand-Nash pricing equilibrium under explicit

production-location assumptions. Under a tariff \((\kappa,O)\), Whirlpool and Maytag reshore

any remaining foreign washer production to the U.S. in year \(t\), while all other firms’ production

locations are held at their year-\(t\!-\!1\) configuration. This mirrors the

domestic incumbents’ ex ante decision problem: rivals’ locations are

expected to persist in the near term, and securing protection is

anticipated to require reshoring by the petitioner.

I compare tariff scenarios to two no-tariff baselines. In the

status-quo baseline, Maytag and Whirlpool’s production

locations remain at where they were in year \(t\!-\!1\). In the incumbent-offshoring

baseline, Whirlpool and Maytag additionally offshore front-loader

production to Mexico in year \(t\)

(top-loaders are not

offshored).Top-loader

offshoring is never observed in the data. All rivals’ production

locations always remain at their locations in year \(t\!-\!1\).

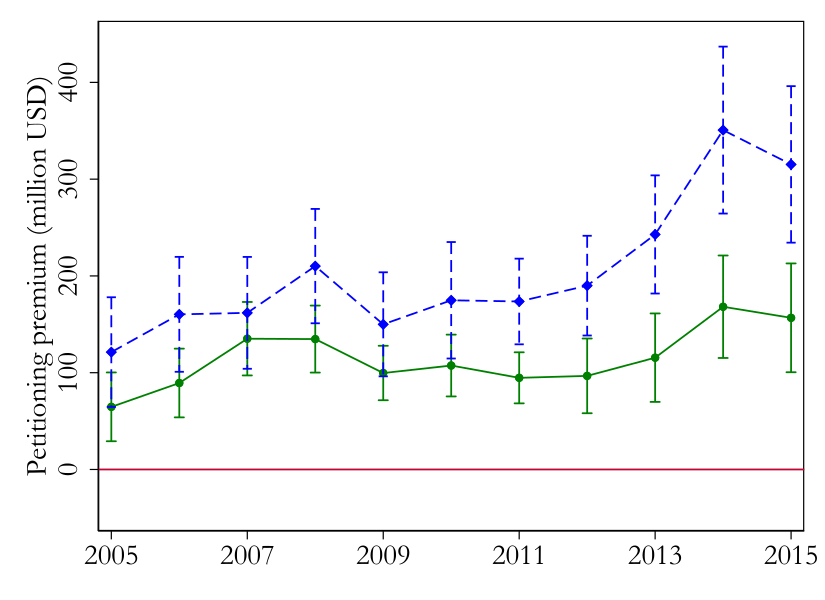

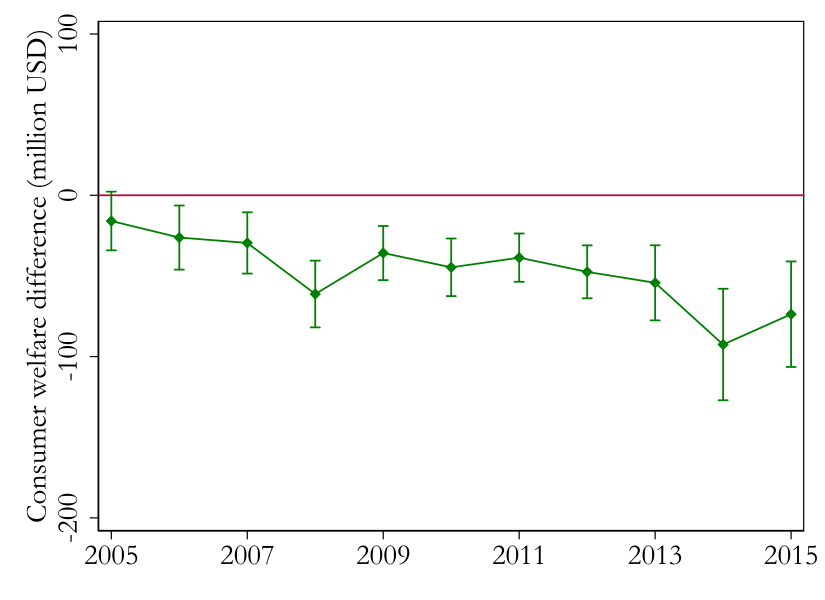

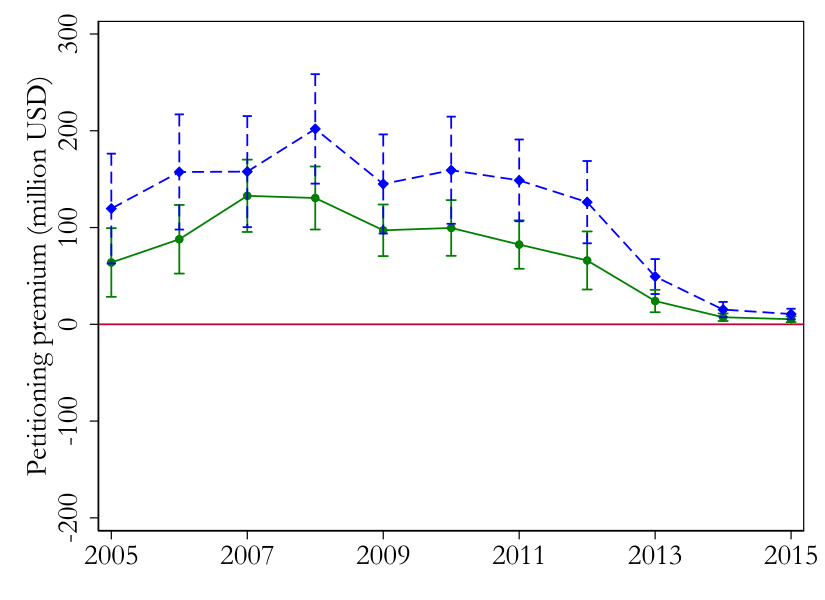

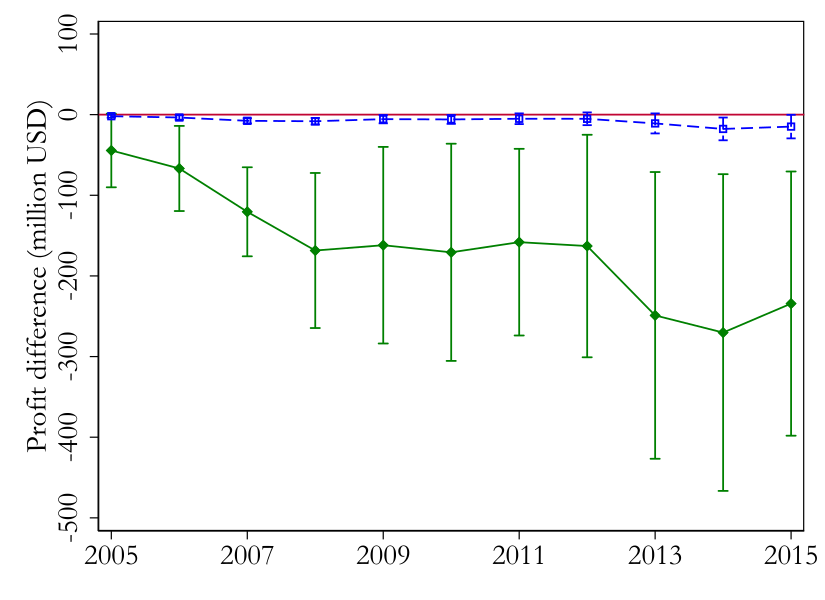

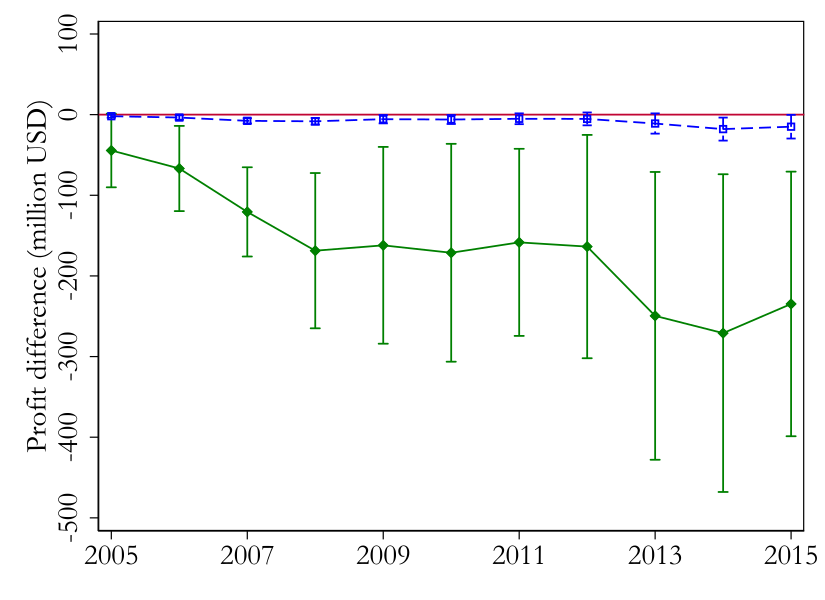

A. Global, status-quo

B. Global, offshoring

Notes: The figure plots Whirlpool’s variable profit from a

\(50\%\) global import tariff relative

to its no-tariff alternative (the status-quo production configuration in

Panel A, offshoring in Panel B), by year, without the merger (solid

green) and under the Whirlpool–Maytag merger (dashed blue). Positive

values indicate that petitioning is more profitable than the alternative

in variable-profit terms. \(95\%\)

bootstrap confidence intervals are obtained by resampling the demand and

cost shocks (\(\xi\) and \(\omega\)) from their empirical joint

distribution within brand.

Figure 3: Domestic merger: petitioning

versus its no-tariff alternative, \(\kappa =

50\%\), global tariffs

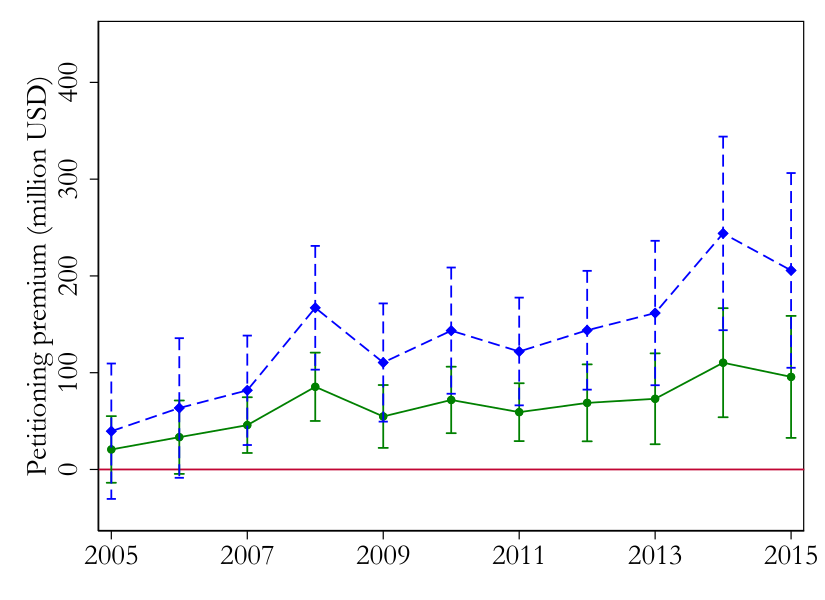

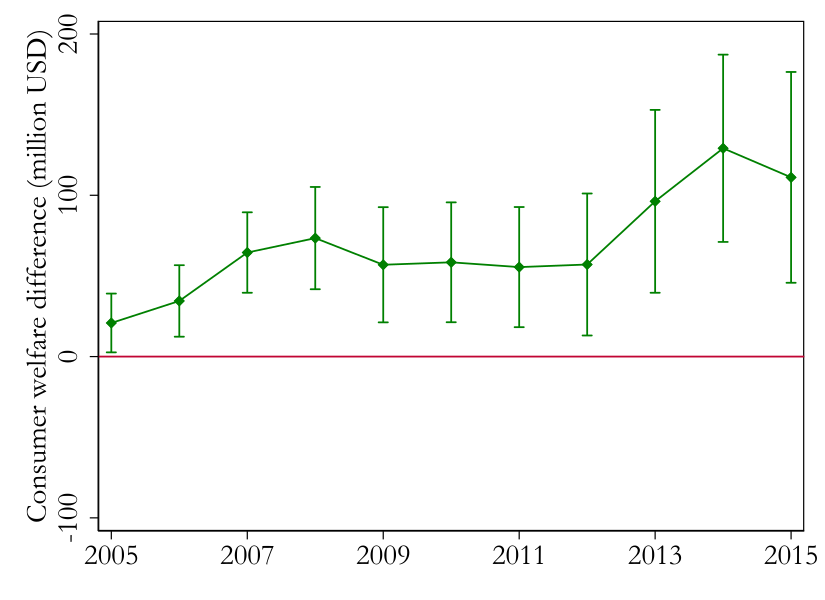

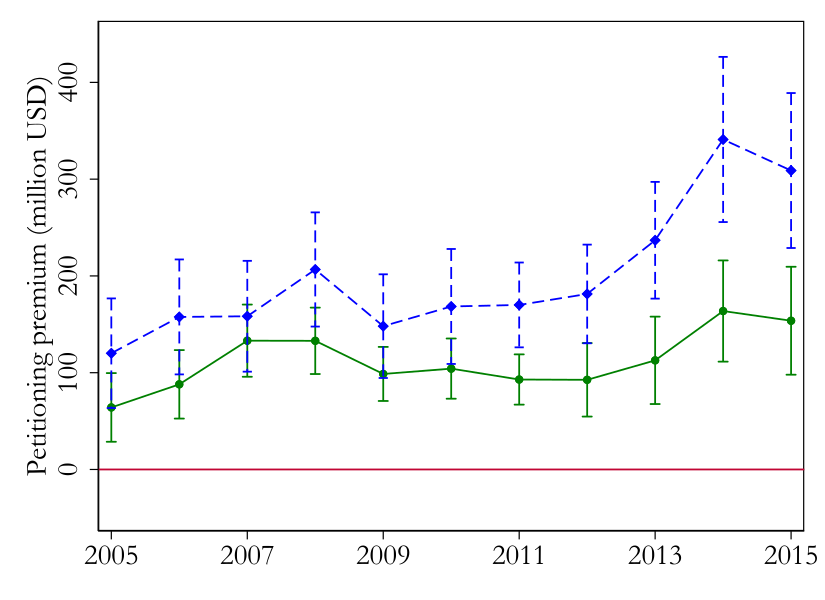

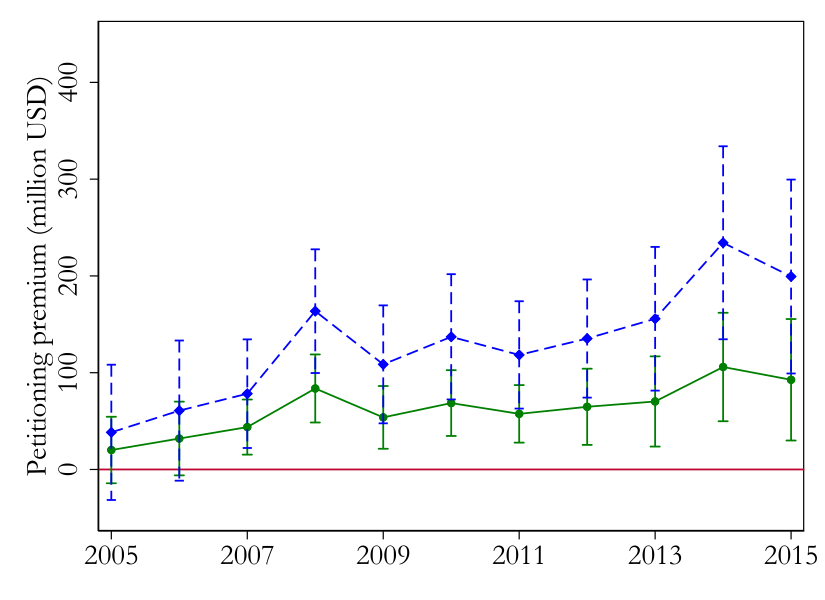

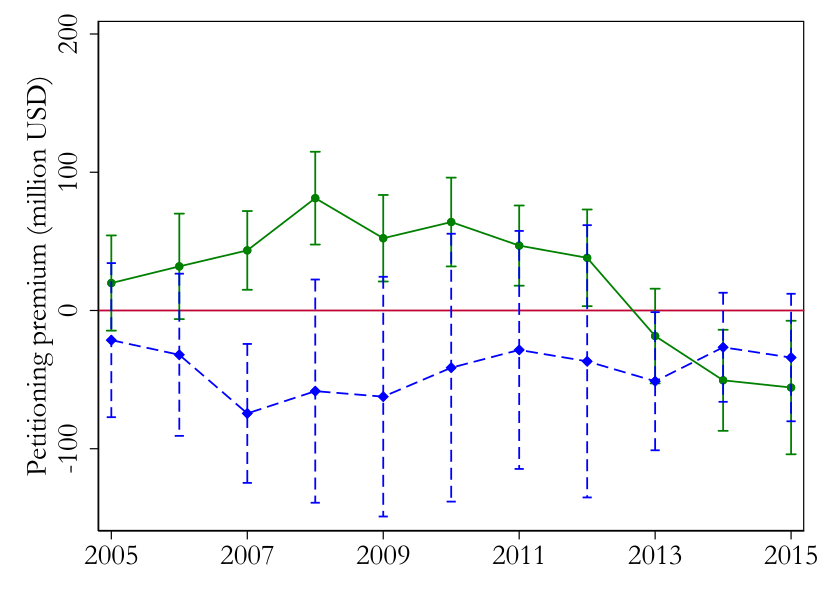

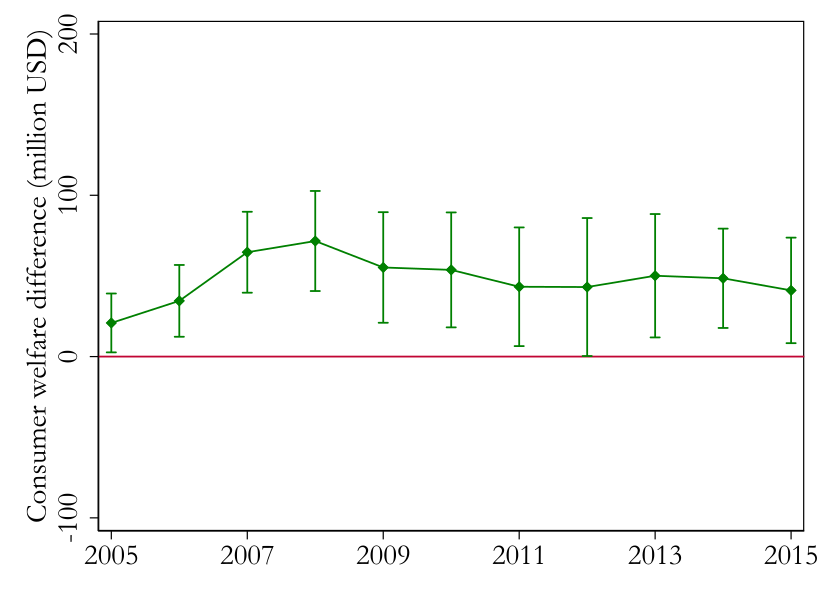

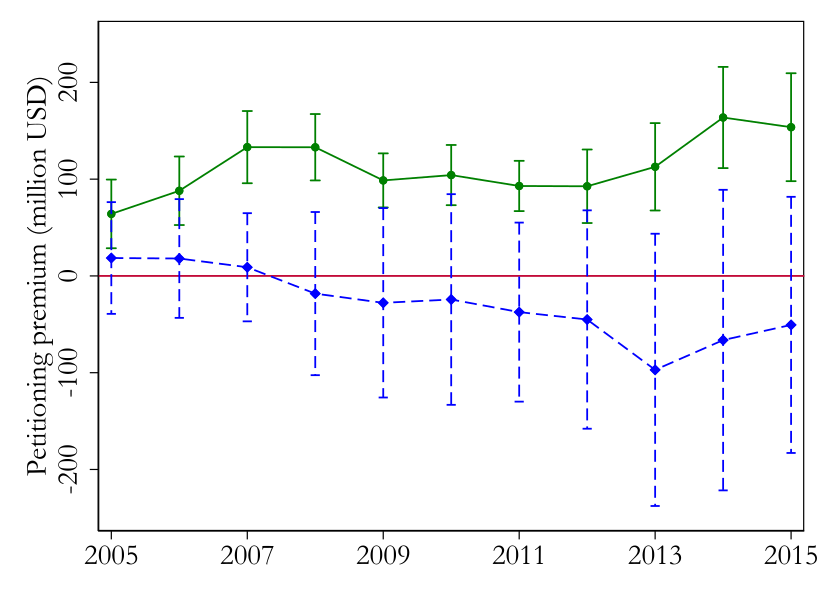

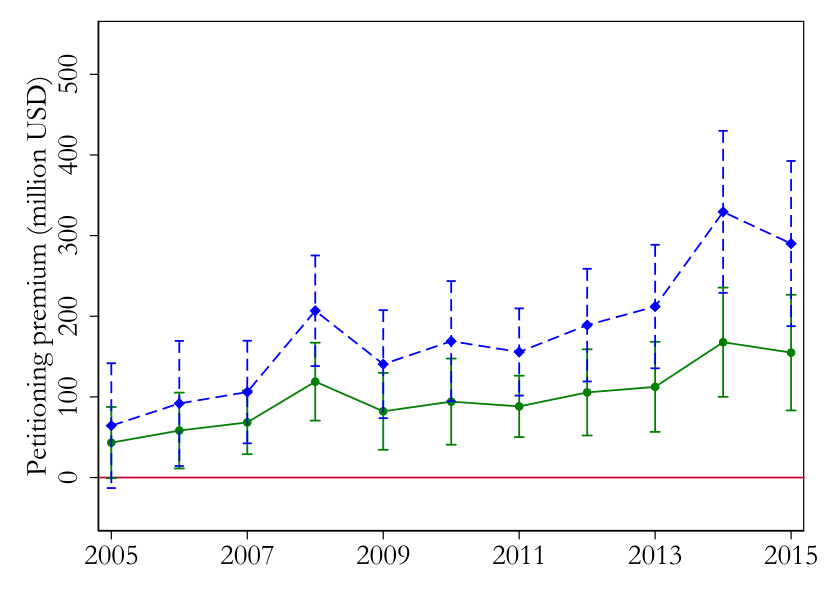

Figure 3 reports the profitability of

petitioning relative to its no-tariff alternative for Whirlpool in each

year, with and without the Maytag acquisition, under two baselines.

Panel A shows the premium of petitioning over the status quo, \(\pi^{\text{pet}}-\pi^{\text{sq}}\). It

becomes immediately clear that if the alternative is the status quo,

then petitioning is highly profitable in variable profit terms and the

merger increases its profitability. However, since the status quo is

dominated by offshoring, the relevant comparison to petitioning should

also be offshoring.

Panel B shows the premium of petitioning over offshoring, \(\pi^{\text{pet}}-\pi^{\text{off}}\). Two

patterns emerge. First, the premium rises as import competition

intensifies, from about $20 million in 2005 to about $95 million in 2015

absent the merger. As the combined market share of LG and Samsung grows

over the period, a tariff that raises foreign costs becomes more

valuable relative to lowering Whirlpool’s own costs through offshoring.

Second, the merger shifts the premium upward in every year. The gap

between the two lines is the merger’s effect on the incentive to

petition, which I decompose into an appropriation and a strategic effect

below.

This comparison is in variable profits and abstracts from the fixed

costs of each option. A \(50\%\) global

tariff is a strong instrument, so the premium is positive throughout the

sample. The figure therefore overstates how early petitioning becomes

worthwhile. Petitioning requires paying the filing cost and reshoring

production to establish standing, whereas offshoring, already under way

by the late 2000s, entailed no further fixed cost. The duties actually

sought in the first rounds were also smaller and narrower than a \(50\%\) global tariff. Net of these costs,

the rising premium is consistent with Whirlpool turning to trade

protection only as import competition strengthened, filing its first

petition in 2011.

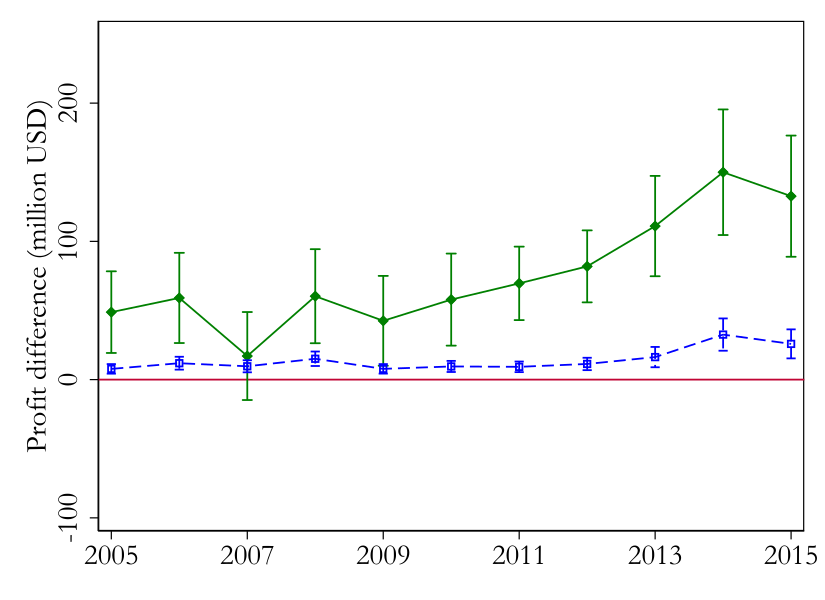

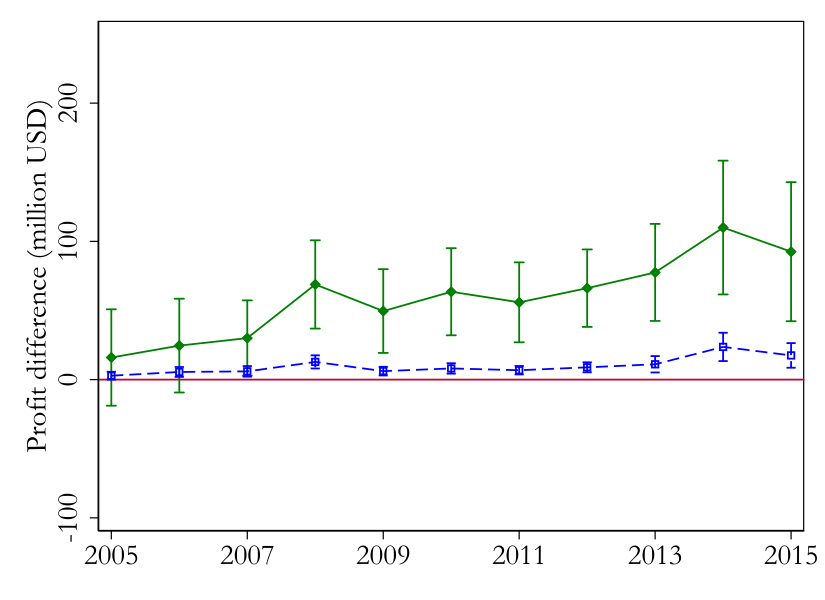

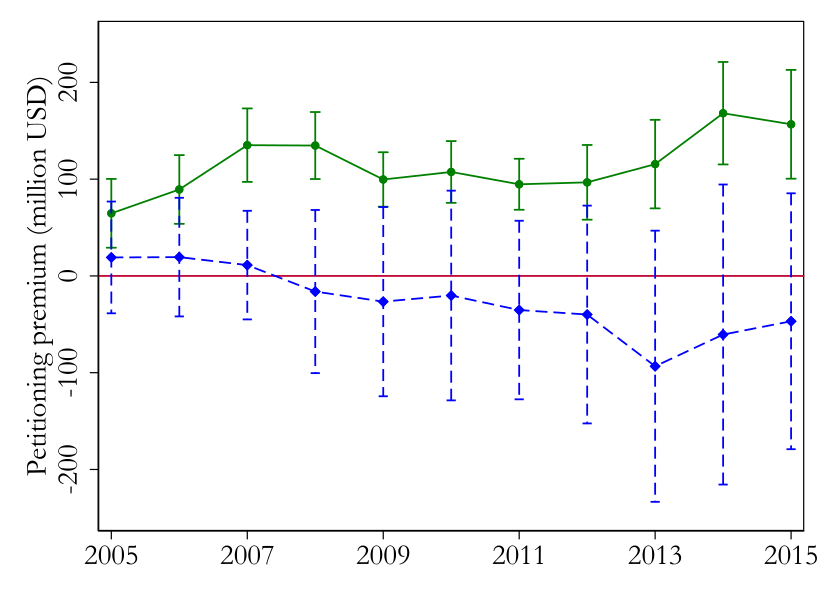

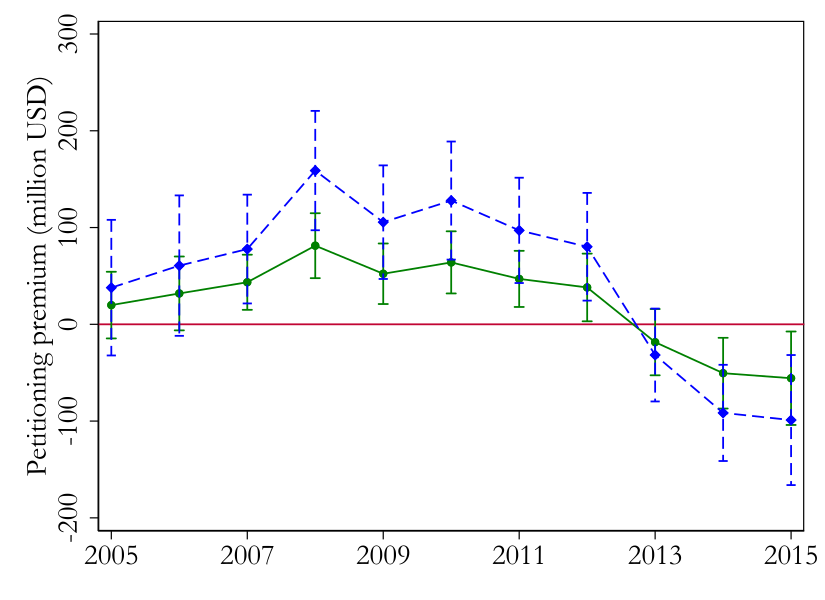

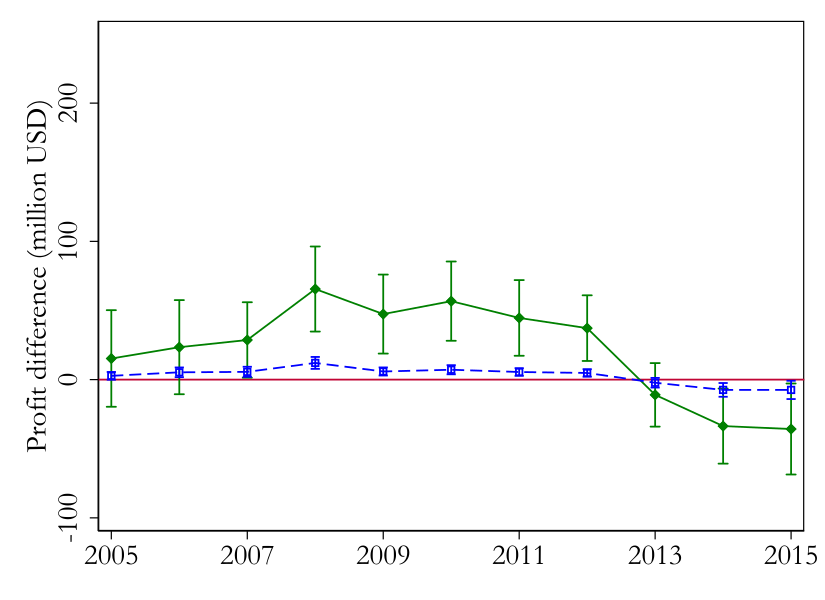

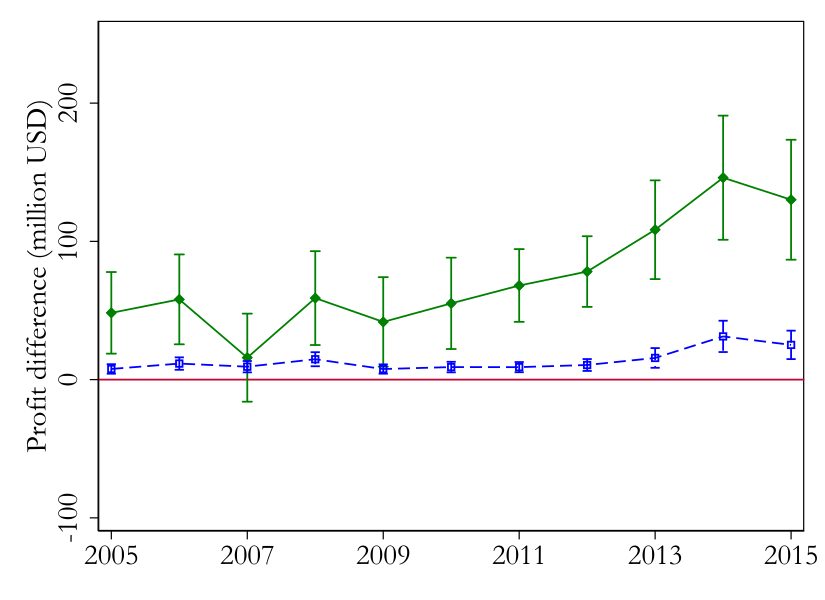

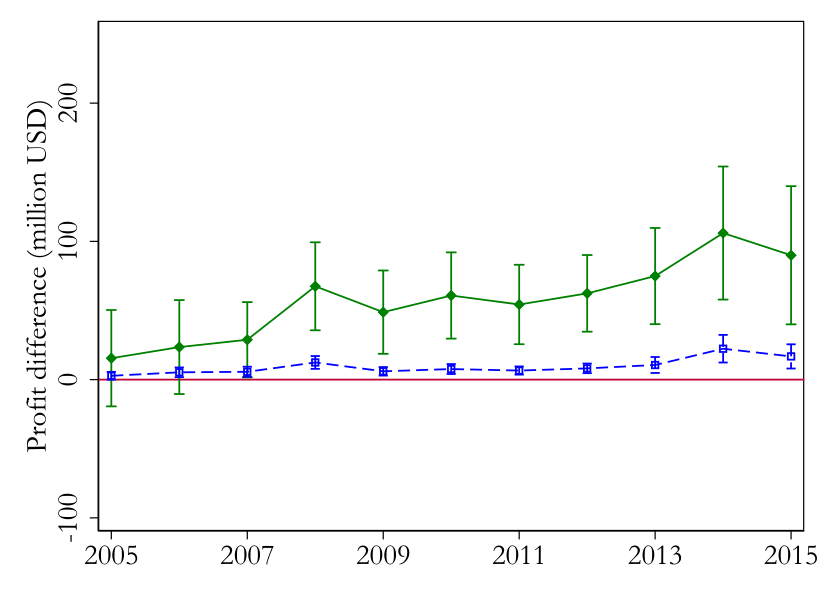

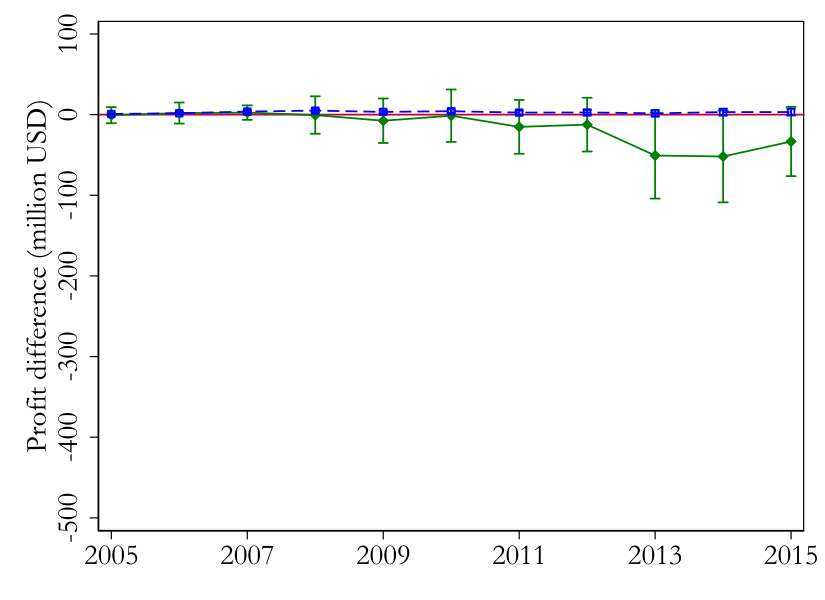

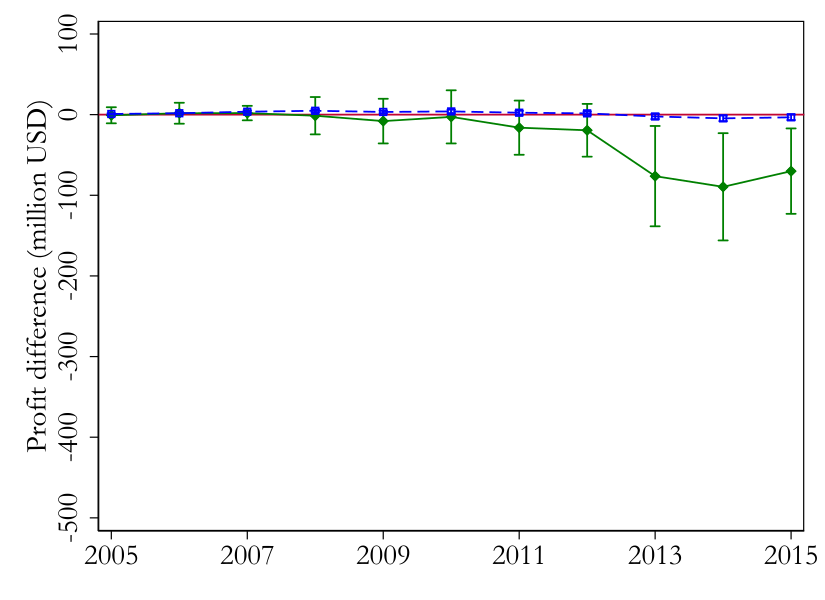

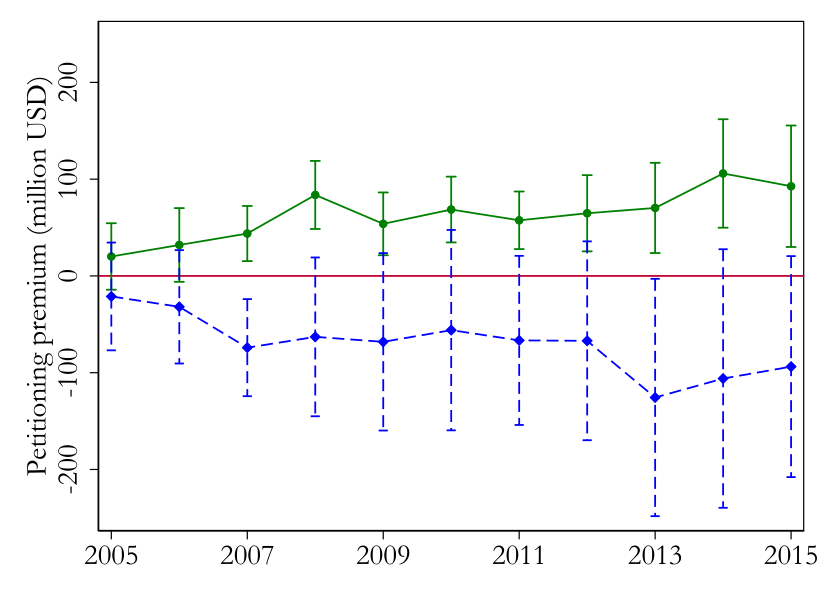

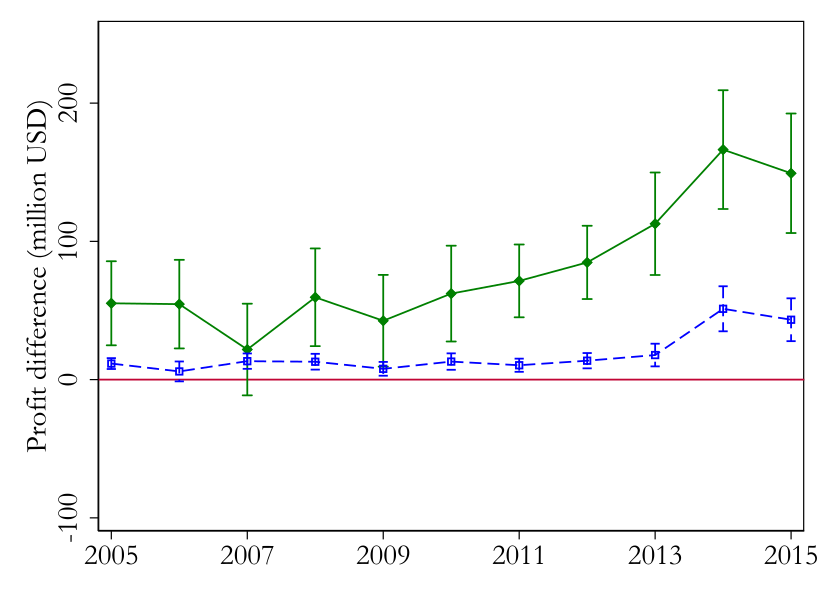

Figure 4 plots the appropriation and

the strategic effect of acquiring Maytag for Whirlpool from a \(50\%\) global tariff on imports of large

residential washers. The panels compare results against the

status-quo baseline and the incumbent-offshoring

baseline.

A. Global, status-quo

B. Global, offshoring